Constellation Software ($CSU) Deep Dive

In 1957, Philip Fisher published the famous book “Common Stocks and Uncommon Profits”, and if you asked me to describe Constellation Software in a phrase, my answer would derive from it: “Boring Software and Uncommon Profits”.

This world-class compounder was founded in 1995 by Mark Leonard, in Toronto, the CEO until the end of 2025, generating roughly 30% CAGR since its IPO in 2006. After a decade working in venture capital, Mark saw a distinct chance in the fragmented vertical market software industry (VMS) that wasn’t attractive enough for VCs due to small TAMs, and not being the hot topic. From this, emerged the opportunity to establish a lasting entity that would acquire, nurture, and grow these specialized software businesses, benefiting from their structural economics, such as the capability of producing above-average free cash flow margins with low reinvestment needs, allowing them to keep buying more companies.

To start this venture, Mark raised approximately $25 million CAD primarily from the Ontario Municipal Employees Retirement System (OMERS), a Canadian pension fund. Additional, smaller investments came from his previous colleagues at the venture capital firm Ventures West Capital. After 30 years, Constellation Software reached a ~$108B CAD in market cap in the 2025 stock all-time-high, earning Mark a seat on the best capital allocators in the world group, alongside Buffett, Munger, Tom Murphy, John Malone, Henry Singleton, among others that you can read in William Thorndike’s “The Outsiders” book. This level of performance was only possible due to the vision of establishing Constellation as a permanent capital vehicle for VMS, contrasting with the “flipper” mindset of Private Equity and Venture Capital, and by deploying capital in smaller, overlooked companies by larger investors, with the goal of never selling them.

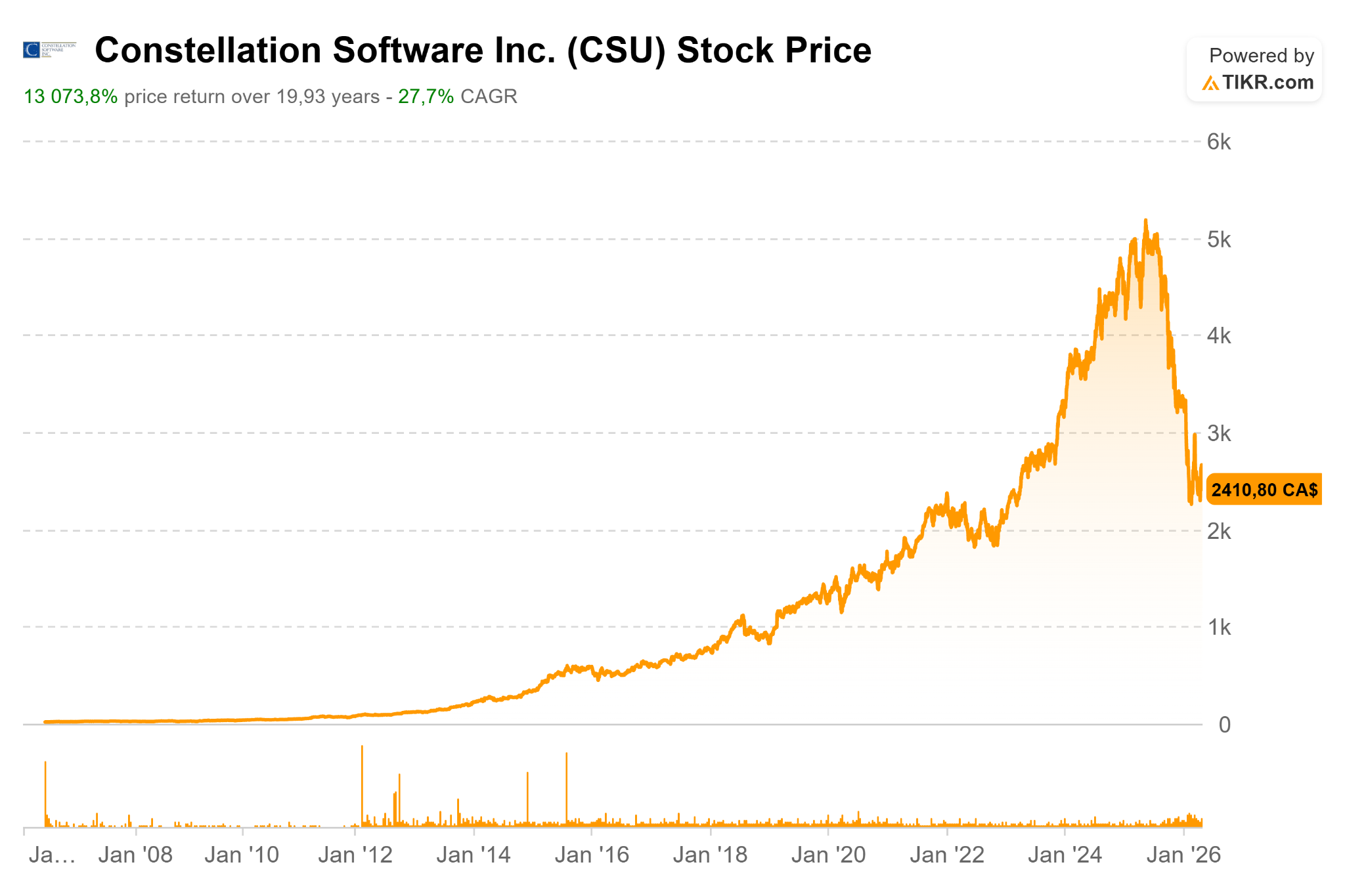

Due to the current “SaaSpocalypse”, Constellation Software stock ($CSU) is down more than 50% from the ATH registered less than a year ago.

The company is now trading as if the clients of each vertical software company will simply use AI to vibe code their way out, leaving behind software that was improved for many years, specifically for their exact niche and market, not to mention the relationship and trust built with each vendor, which most likely leads them to delegate AI implementation rather than disruption, creating a new opportunity to upsell on existing clients. Despite that, the stock is now trading at a historically low valuation, as if AI will take its entire business model, and these moments where investors get irrational are when opportunities emerge. Nonetheless, it might take a few quarters for the market to realize that Constellation Software and its subsidiaries aren’t going anywhere.

Simply come to your own conclusions: Do you think there’s a chance that a marina, or golf club, that has worked with a vendor for 10+ years, will simply spend their time vibe-coding, fixing bugs, and spending a lot of money on AI tokens just to try to replicate a software that’s been constantly improved to their exact business, with their data, to precisely fit their needs, and save 0.5% of their revenue in software costs?

The Business Model Explained

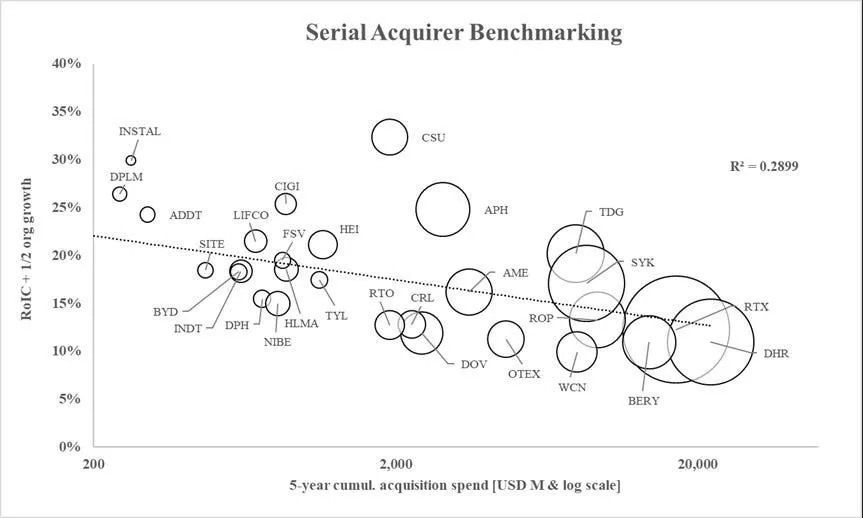

Constellation Software ($CSU - listed on Toronto Stock Exchange) is a serial acquirer of Vertical Market Software (VMS) companies and a permanent holder of them, one of the most unique holding companies ever existed. Usually, holding companies serve as vehicles to diversify investments (Berkshire Hathaway and Fairfax Financial Holdings, founded by Prem Watsa, the “Canadian Warren Buffett”, are classic examples), but Constellation follows the exact opposite by exclusively focusing on VMS companies and staying in this lane for decades, something that might be changing due to the “law of large numbers” and the need to look at other markets to keep generating strong returns on investment. Constellation Software owns over 850 to 1,000+ companies, acquired since 1995. They focus on software companies in the small-to-mid market segment, generating <$20M in revenue. The business model can be described as “Permanent Private Equity” because they don’t exit companies like Private Equity does in the traditional sense.

What is Vertical Market Software (VMS)

VMS is specialized software designed for a specific industry or niche, addressing unique workflows, regulations, and needs, rather than general business functions. VMS offers high customization, deep industry functionality, and high customer loyalty, distinguishing it from “horizontal” software like Microsoft Office or Salesforce. Common sectors include healthcare, construction, and legal, with cloud-based solutions dominating the market. It usually benefits from higher user retention when compared with the horizontal counterparts.

How Constellation Software Makes Money

Constellation Software generates revenue in an unusual — but powerful — way. It’s less like a traditional software company and more a decentralized holding company for hundreds of niche software businesses. Its subsidiaries earn money through the usual SaaS subscriptions/license fees, maintenance & support, professional services (for example consulting, implementation, training or customization), and transaction fees in some verticals. VMS companies have the structural advantage of high retention rates (approximately 72% to 75% of Constellation Software’s revenue is recurring) due to multiple factors, some of them are the switching costs that come from having to spend resources training personnel in order to change to a competitor’s solution, and the deep workflow integration, vertical SaaS is usually customized to fit each client in perfection. Through their growth engine, acquisitions, Constellation applies the playbook of buying a company, improving it modestly, and harvesting cash flows to finance the next acquisition — it just keeps compounding — so revenue is also acquired, and doesn’t come only from organic growth. Their product isn’t software, it’s capital allocation.

Conglomerate Structure

Since Constellation was founded, Mark never followed the herd. Despite coming from a venture capital background, the vision has always been to build a permanent capital vehicle, not looking to invest in the early days and exit for a large return years later, but to buy and hold vertical software firms forever, the ones that are already profitable and have paying clients. This is extremely uncommon and can only be compared to what Buffett and Munger built on Berkshire Hathaway.

VCs look for high-growth, scalable startups, also in technology sectors, with large total addressable markets and early traction. This leaves a blank space for the software companies operating in very small niches, without much margin to grow further, but being profitable and with high free cash flows, the profile of VMS companies.

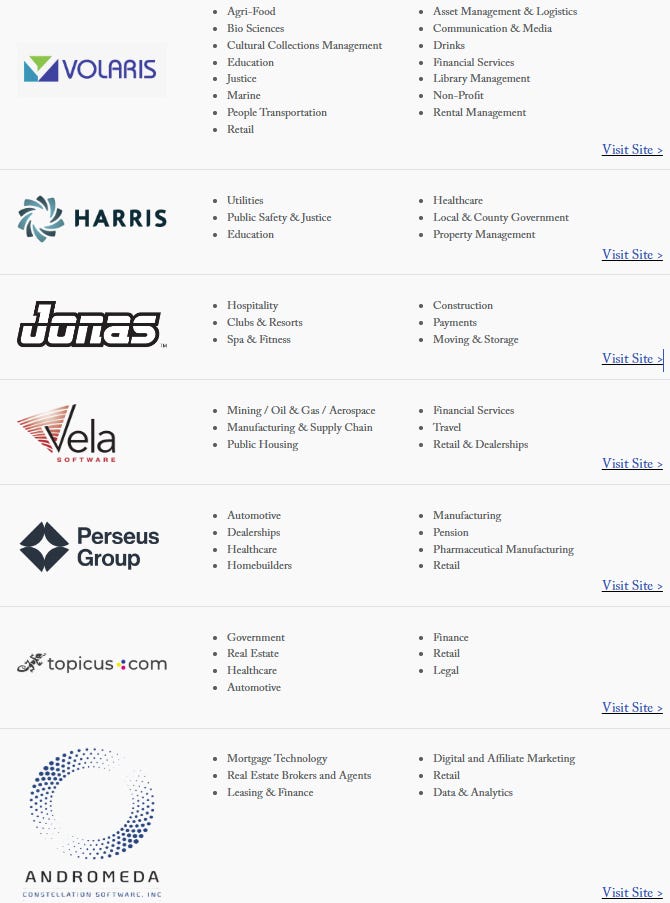

Unlike most conglomerates that look to centralize most decisions, Mark also does the exact opposite, allowing a high level of decentralization for the executives managing each operating group and business units. Operating groups don’t need head office approval for acquisitions up to $20M, although the capital allocation discipline doesn’t go away, the reputation for applying high, disciplined internal rates of return (>20%) is there. The holding is structured in 7 operating groups for different market verticals:

Acquisition Pillars

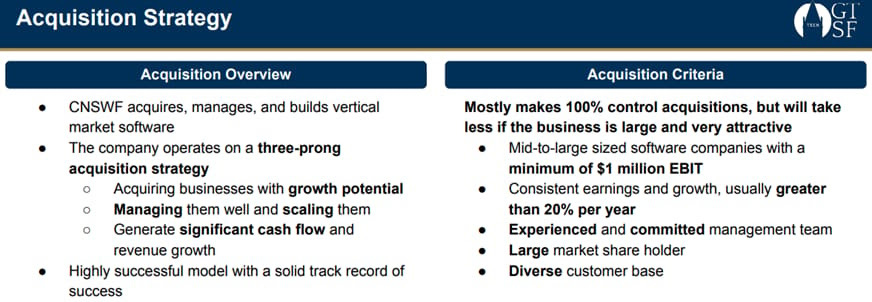

Niche Vertical Market Focus: CSU acquires VMS businesses that are market leaders (#1 or #2) in specialized, overlooked niches, making their software essential to customers. Most companies are below $20M in revenue, so financial institutions don’t touch them.

Decentralized Engine: Seven primary operating groups (Volaris, Harris, Jonas, Vela, Perseus, Topicus, Andromeda) operate autonomously, enabling over 100+ acquisitions annually.

“Buy and Hold” for Life: Acquisitions are rarely sold, treated as permanent investments to cultivate long-term cash generation and use it to fund further acquisitions.

Strict Financial Criteria: Targets must have proven profitability (often minimum $1M EBIT), strong management, and high recurring revenue.

Proprietary Sourcing: A database of 40,000+ potential targets allows for proprietary, direct-to-owner outreach, minimizing bidding wars.

Founder Independency: CSU is recognized for preserving the culture and brand of acquired firms, allowing founders to remain and run the business with autonomy.

Compensation, Incentives & Management Team

In Constellation Software, compensation structure is also different from what we are used to see in most other public companies. Compensation and bonuses are based upon the profitability and revenue growth of the operating group or business unit.

The long-term focus is accomplished by mandating that at least 25% of the compensation of the majority of senior employees who earn in excess of $75,000 per annum, and have bonuses in excess of $10,000 per annum, be reinvested in shares of the company that are subject to restrictions on resale for a period of three to ten years. At a minimum, these restrictions require employees to hold 100% of their shares for the first two years, and then one third of such shares may be sold in each of years three, four and five. Senior executives are required to invest 75% of their bonus in shares of the Company that are subject to the same restrictions on resale for a period of three to ten years. Once every five years, employees may elect to receive 100% of their bonus in cash.

Mark Leonard owns roughly 1.85% of Constellation and Mark Miller (current CEO) owns 1.2%. Mark Miller has a total compensation of $1.85M, likely salary + bonus. Bonus is tied to ROIC (net of a hurdle rate, historically 5%) and growth (not conventional EPS targets), also there’s mandatory reinvestment of much of the bonus into CSU stock. Miller reportedly owns roughly 1.2% of Constellation, worth hundreds of millions (around C$640M / US$466M depending on source timing), which tells us that compensation comes from incentives in equity compounding, not annual paychecks, perfectly aligned with shareholders.

Management Team

Constellation Software is in a CEO transition, from the founder and world-class capital allocator Mark Leonard to Mark Miller. I view this as a positive decision, Miller has decades of experience inside the Constellation ecosystem, he’s a strong choice for someone to continue applying Mark Leonard’s playbook, especially in a time where the company is transitioning into larger deals due to the “law of large numbers”.

Founder - Mark Leonard

Founded and ran the company from 1995 to 2025

Former venture capitalist (~11 years) before starting the company

MBA from Western Ontario; science background

Famously reclusive and media-averse

Often compared to Warren Buffett for capital allocation discipline and long-term ownership mindset

Stepped down as President in 2025 (health reasons)

Left the board in 2026 and moved into an advisory role (PEMS strategy)

Current CEO - Mark Miller

With Constellation ecosystem for 30+ years

Former COO, now President

Co-founded Trapeze Group (one of CSU’s first acquisitions)

Strong operator and manager developer

Seen as a continuity leader, not a strategic disruptor

CFO - Jamal Baksh

Capital allocation partner to the operating groups

Ensures:

return thresholds are met

capital is tracked and redeployed efficiently

CIO - Bernard Anzarouth

Leads investment strategy and acquisitions

Central figure in evaluating:

large deals

portfolio capital allocation

Think of him as a portfolio manager inside the firm

SVP, Large Acquisitions - Farley Noble

Focuses on bigger, more complex deals

Handles the segment where decentralization doesn’t fully apply

Important as Constellation moves into larger acquisitions

Competitive Moat & Risks

Constellation Software has a wide moat that can be divided in two parts, VMS companies, and Constellation the conglomerate itself.

Starting from the VMS side, these companies derive their competitive moat from being deeply embedded in operational workflows for a specific industry, usually with the software customized to the needs of each company, creating high switching costs, and controlling specialized data. While horizontal software offers broad functionality (such as general CRMs), VMS is the backbone for niche industries like construction, restaurants, or healthcare. VMS is rarely just a tool, it’s often used to run entire full operations, including POS, payroll, and compliance. Replacing these systems requires enormous effort in data migration, process re-engineering, and staff retraining, making customers highly hesitant to leave. Providers of these softwares accumulate unique data on how their customers operate, enabling them to build superior predictive insights or specialized AI models that generalists cannot. On VMS companies, AI disruption is a real thing for softwares that are a thin UI over standard data, which is not the case for companies the Constellation acquires, these are market leaders in their niches.

On the conglomerate side, I think Mark exaggerated a bit when he famously said that “the only barrier to starting a software conglomerate is a phone and a chequebook”. Constellation benefits not only from the intrinsic moat of each VMS company itself, but also from the diversification, if one business is in a decaying segment, the conglomerate as a whole won’t have a material loss. Besides that, the company also has the decentralized model, hundreds of small business units operate autonomously, allowing them to remain agile and close to customers, which when combined with the respect for the employees and each company’s culture, makes Constellation the preferred buyer for niche software founders that end up accepting lower valuations than Private Equity would offer them, in what they consider worse post-acquisition conditions.

Risks

Despite trusting that Miller’s 30-year education under Mark Leonard makes him a strong choice to drive CSU further, we need to acknowledge that there’s a key-man risk. The company was founded and ran by Mark Leonard for three decades. Every system, incentive, vision, culture, and capital allocation came from his head; we still don’t know if Miller will drift away from something the shareholders have been used to.

Constellation got to a size that makes acquisition of small VMS hard to move the needle. To some degree, conglomerates aren’t scalable. Capital becomes harder to deploy at high rates of return as the cash pile gets larger. Deals get more competitive at higher valuations and multiple arbitrages are harder to find.

To avoid future lower returns, management already signaled some important shifts that include delving into verticals outside of VMS, using more leverage to stay competitive with Private Equity, start returning capital to shareholders if there aren’t opportunities that meet hurdle rate requirements, and building the public company portfolio. Mark Leonard specifically spoke about the risk of Private Equity driving up acquisition prices and lowering IRR:

“Externally, competition to buy vertical market software (“VMS”) businesses is intense. Vista Equity Partners and Thoma Bravo are two of the most prominent private equity (“PE”) firms that concentrate on software acquisitions. Roper Industries is a large publicly traded industrial conglomerate that we included in our HPC study and that also actively competes for VMS acquisitions. Vista currently manages approximately $28 billion of capital and Thoma Bravo is managing approximately $16 billion… In the last 9 years, Roper Industries has invested five times as much capital in the VMS sector as CSU has since its inception, 22 years ago”.

Another risk I want to emphasize is the difficulty in growing organic revenue. VMS operates in very tiny, niche markets that are too small to attract competition but also to keep expanding. Since 2008, CSU demonstrated an organic revenue growth just in line with inflation, which is expected in this business model, most software companies already saturated their small market, and this can only be compensated with further acquisitions.

And the last one, AI disruption concerns, the cause of the current turmoil. This is a real threat, and I can’t say that 100% of subsidiaries are safe from disruption. VMS is highly targeted and specific to the company and niche, but the threat of AI-driven alternatives is real.

The Spin-off Strategy

Spin-offs together with an acquisition allow Constellation to target companies that couldn’t be acquired under the holding for a variety of reasons, such as valuation or culture. The decision to spin-off fast-growing operating groups, such as Topicus and Lumine Group, is value-unlocking for shareholders, it leads to a valuation premium as the spin-offs often trade at higher valuations than the parent company, highlighting the value of focused, fast-growing assets. These movements allow for aggressive acquisition strategies, often using rollover equity to acquire larger targets without exhausting parent company cash, while keeping control via preferred shares and maintaining access to CSU’s best practices in capital allocation. At the current size of CSU, starting to give some independence to the operating groups is terrific way to create wealth for shareholders due to the multiple expansion, keeping the culture and management incentives aligned with long-term growth, the exact playbook we are used to since 1995.

Lessons for Investors & Operators

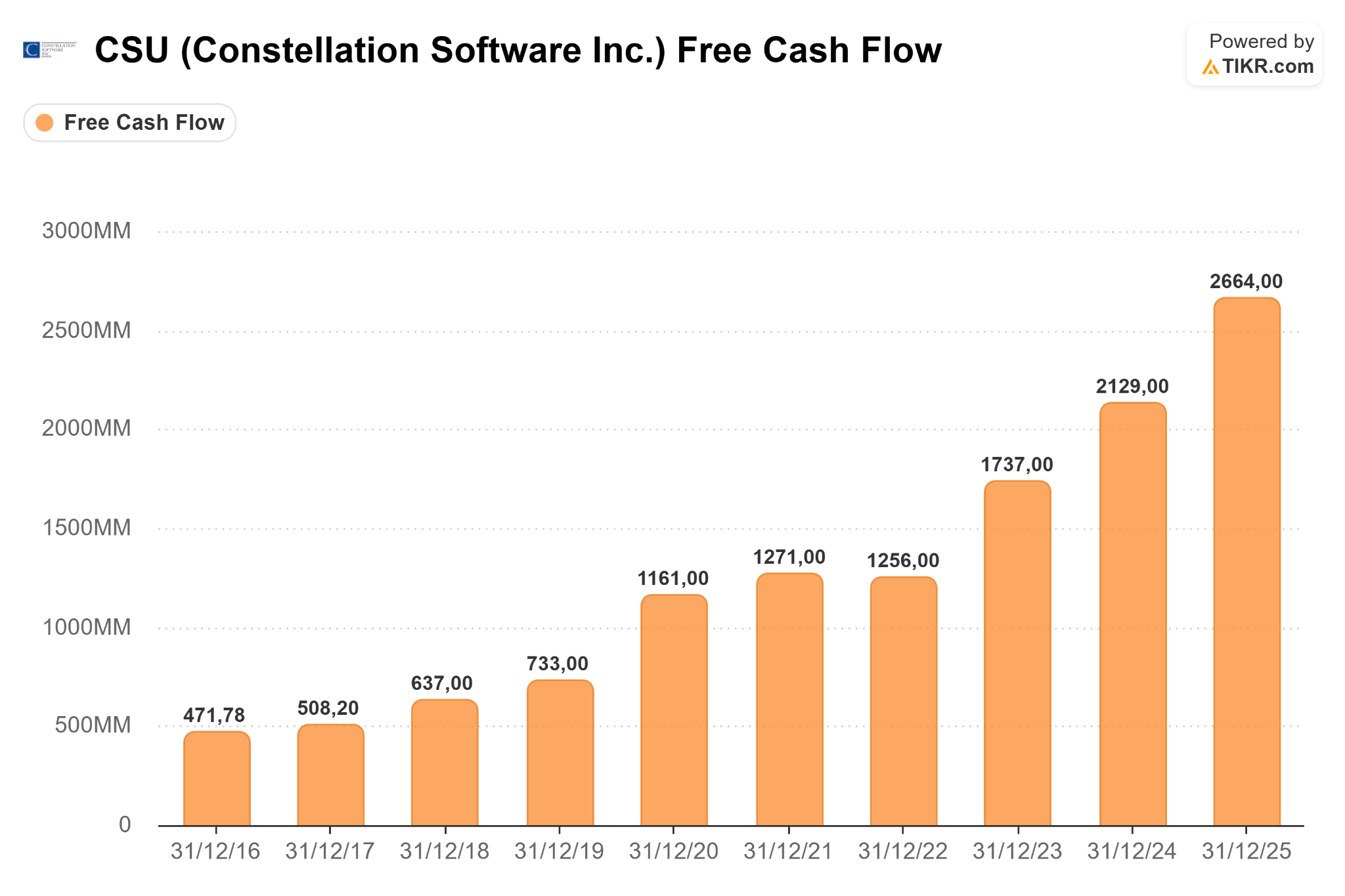

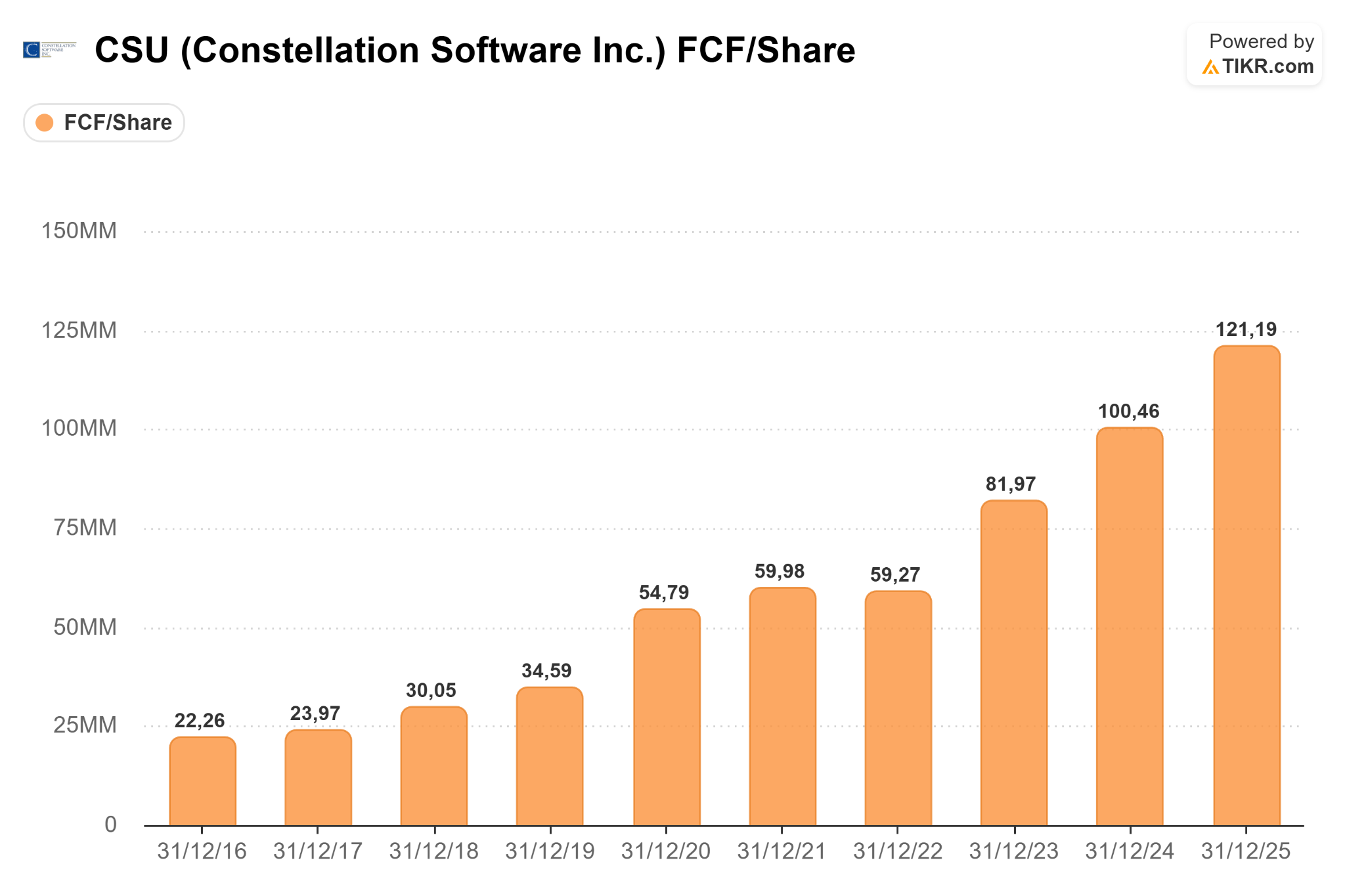

Management decisions that led a company to generate a 27.7% CAGR in the stock price for almost 20 years, even with the recent “SaaSpocalypse” dip, together with a 18.9% CAGR in Free Cash Flow in the last decade, is something that needs to be studied for investors and business owners, we can learn capital allocation at a level that’s not taught in any business school. So, I decided to dedicate a section of the deep dive for the main lessons we get from Constellation Software’s stellar performance.

Decentralization and Delegation: Everyone talks about the importance of delegation in business, but very few master it, only the ones that build real, scalable companies with enterprise value, instead of a well-paid job. Constellation supports its acquisitions with capital, and the best practices of management and capital allocation, but keeps its management team in place, existing culture, and a lot of autonomy. When we hire smart people to do their jobs, we shouldn’t let our egos get in front of the decision-making process because of thinking that the spotlight is ours. In the end, the only thing that matters is growing the company’s revenue and free cash flow, the combination that leads to an increase in the shareholders’ wealth. The most capable people should occupy their respective positions without being micro-managed.

Focus on the circle of competence: Constellation’s north star has always been to acquire Vertical Market Software (VMS) companies that dominate their respective markets and generate real cash flows, not large mainstream software firms nor betting in new enterprises that have a high “potential” but don’t produce cash, the typical speculative VC playbook. One example is the acquisition of Allscripts Hospital EHR business, in 2022. This company focuses on healthcare and helping medical facilities manage their operations, dominates its niche and has a moat, the kind of purchase Mark Leonard always looked for.

Measuring capital allocation in ROIC, not the traditional EPS that become an accounting gimmick: Constellation makes almost all acquisitions without debt. It uses existing companies’ cash flows to acquire more, creating a self-perpetuating money-printing machine. The company looks for a high ROIC in its investments, with acquisitions following strict hurdle rate rules based on size:

< $1M Revenue: ~30% IRR.

$1M - $4M Revenue: ~25% IRR.

Large Deals (> $100M+): ~20% IRR (can drop to 15% for very large, rare deals)

To deploy increasing amounts of capital, CSU uses the Permanent Engaged Minority Shareholder (PEMS) strategy to purchase stakes in larger, publicly traded vertical software companies while still targeting their mandated hurdle rates.

Power of incentives: CSU’s stock performance is a textbook example that executives achieve extraordinary results when they’re shareholders, looking to see their wealth grow together with the non-executive ones, instead of being focused on the next salary raise; simply trying to extract the most amount of money in the short-term while damaging the long-term picture. Mark Leonard resisted taking the company public because the investors’ focus on short-term price movements, the loss of autonomy, and persistent analyst scrutiny, could end up harming the conglomerate’s performance.

Financials

The only thing that ultimately matters for an investor, independently if you’re buying shares in public or private companies, is the free cash that this endeavor will allow you to receive. A 10-Year FCF/Share CAGR of 18% is why people call Constellation Software a compounder. This level of performance is only seen in quality companies, the select group of wonderful businesses that have their stocks public, the ones that we dedicate our time studying and investing in.

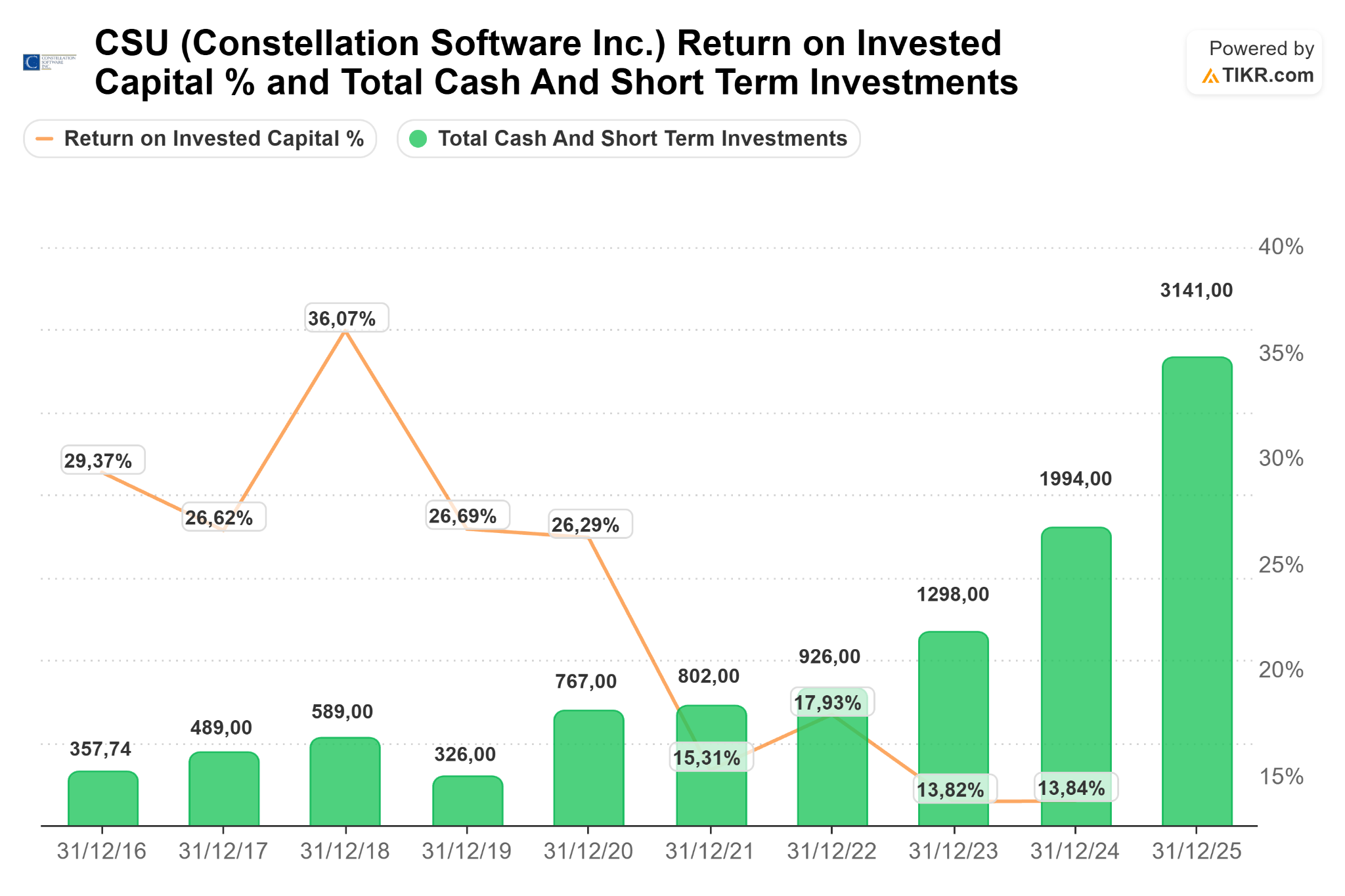

Next, I want you to take a look at the ROIC and Total Cash & Short-Term Investments trend, it visually demonstrates the constraints that a large conglomerate faces when deploying capital. As capital grows, acquisitions get more competitive (private equity bidding) which leads to higher multiples that need to be compensated by higher returns, this not always happens. The universe of high-return targets shrinks, margin dollars earn less than early dollars, and the company starts accumulating more cash as the opportunity window shrinks. This trend can have a reversal if a considerable part of this dry powder is deployed in new acquisitions at historically low multiples. In multiple shareholder letters, Mark Leonard emphasized that SaaS companies most often trade at expensive prices, that’s not the current scenario.

Valuation

In the most conservative scenario, CSU’s intrinsic value is ~$3,960/share, which compared to the current price of $2410/share gives us an upside of 64%. Here are the valuation assumptions:

10% 5-Year Revenue CAGR driven by 3% organic growth plus 7% inorganic growth, driven by acquisitions.

In the past 5 years, organic growth stayed in the 3-5% range, so using the lowest percentage is the most conservative assumption.

Inorganic growth at just 7% takes into account that many VMS companies can go out of business due to AI disruption, as this metric has been around 15% for the past years. I consider this projection extremely conservative due to the fact that only a small number of companies might get disrupted, and the current depression in SaaS multiples allows Constellation to start being more aggressive on acquisitions, benefiting from a record level of cash & short-term equivalents, more than $3B, plus the high free cash flow. At lower valuations, these new companies can generate strong returns once the market re-rates them.

Expenses might grow at a slower pace than revenue due to AI productivity gains in software development.

Conclusion

Philip Fisher opened this deep dive, so let him close it too. Constellation Software is exactly the kind of business he wrote about — durable competitive advantages, exceptional management, and the ability to reinvest capital at high rates of return for decades. Mark Leonard found that business hiding in plain sight, in the most unglamorous corners of the software industry, and spent 30 years proving everyone who ignored it wrong.

And yet, here we are in April 2026, with the stock down more than 50% from its all-time high. The market has decided that a golf club in Ohio or a transit authority in Belgium is going to fire its software vendor of 12 years, stand up a vibe-coded replacement, migrate decades of proprietary data, retrain its entire staff, and do all of this to save a rounding error on its operating budget.

The fundamentals haven’t moved. FCF per share has compounded at 18.9% annually over the last decade. The company sits on over $3 billion in cash, ready to be deployed into a SaaS market now trading at some of the lowest multiples in years. Constellation is a predator, and the “SaaSpocalypse” just stocked the pond.

The risks are real — ROIC compression, organic growth stuck at inflation levels, intensifying acquisition competition, and yes, some AI disruption across the portfolio. I’m not dismissing any of them. But at ~$2,410 per share against a conservative intrinsic value of ~$3,960, the margin of safety is wide enough to act.

Constellation Software is being added to the portfolio.

Not because the next two quarters will be clean. But because 30 years of evidence shows this company finds a way to keep compounding — through dot-com crashes, financial crises, pandemics, and now this. The system outlasts the noise.

Boring Software. Uncommon Profits.

Disclaimer: Margin Valley Research is an independent research publication focused on macro analysis and equity research. All content published on this Substack is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security or financial instrument.

The views expressed are solely those of Margin Valley Research and are based on sources believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy or completeness. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal.

Nothing published here should be construed as the provision of personalised investment advice. Readers should conduct their own due diligence and consult with a qualified financial adviser before making any investment decision.

Margin Valley Research may hold positions in securities or instruments discussed in its publications. Any such positions will not be disclosed on an individual post basis and should not be interpreted as a conflict of interest.

This publication is not regulated by any financial authority. By reading this content, you acknowledge that you do so entirely at your own risk.