Meta Deep Dive: The World's Attention Machine Is on Sale — But Is It Cheap Enough?

Every decade or so, the market offers a chance to buy a leading, profitable business at a price that feels uncomfortable. That discomfort is often the point.

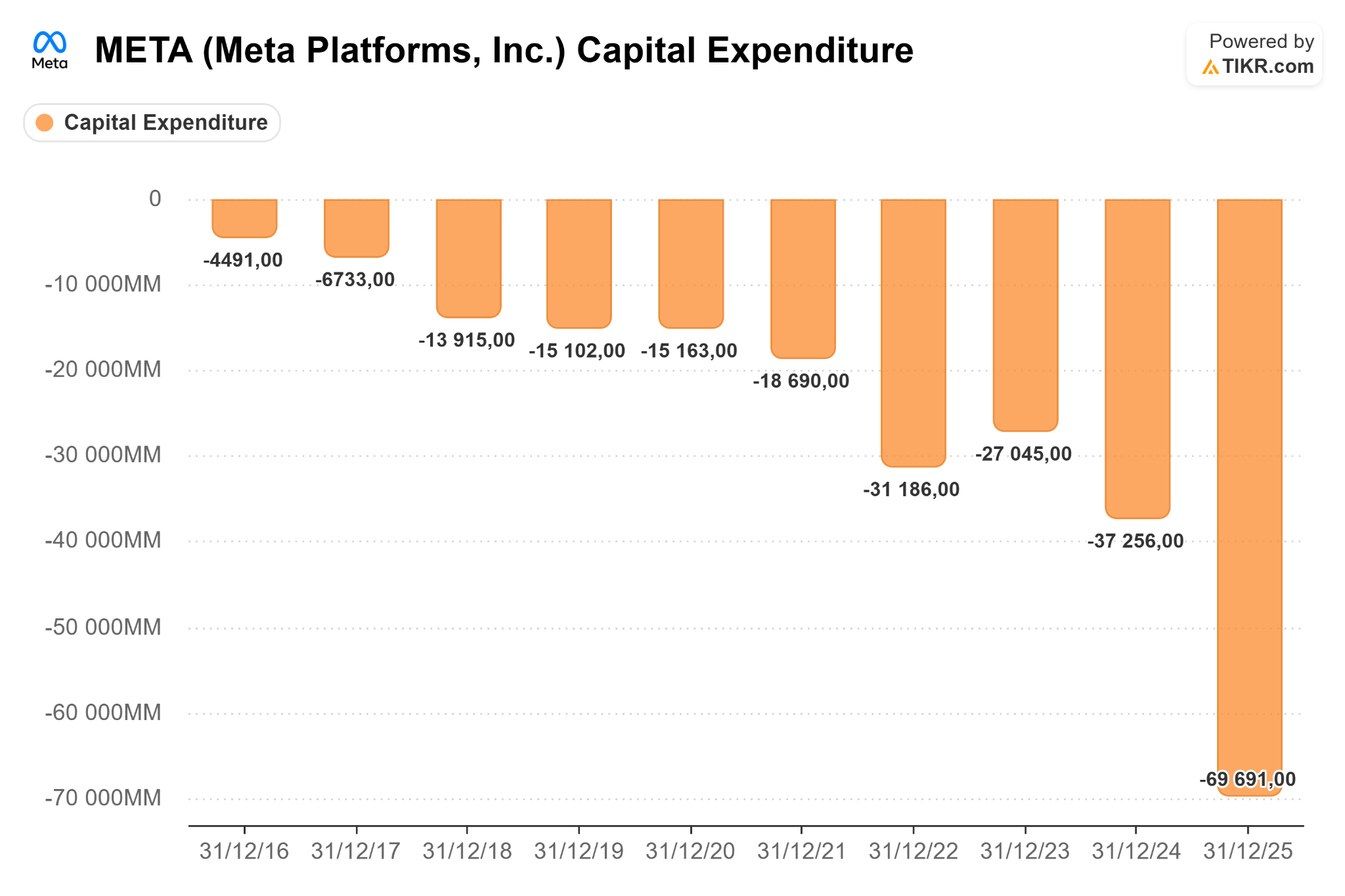

Right now, Meta is going through its largest capital investment cycle ever. Management has projected $115 to $135 billion in infrastructure spending for 2026 alone; that is nearly four times what the company spent just two years ago. The market reacted negatively to this news. The stock dropped sharply, and sentiment around the company has been cautious since then.

However, the market seems to be overlooking some key facts. Meta has 3.27 billion daily active users, a 22% revenue growth rate over the last decade, operating margins consistently above 40%, and more than $80 billion in cash on its balance sheet. It doesn’t need to issue new shares or take on much debt to fund this investment cycle. The company is paying for this with its own funds while still generating positive free cash flow.

The question isn’t whether Meta is a strong business, it clearly is. The real question is whether the current price reflects everything going well, and what will happen to our returns if it doesn’t.

In this deep dive, I will explain what Meta really does and how it makes money, why its competitive position is stronger than many people think, how management has earned the authority to make large unconventional bets, and what the business is realistically worth in different scenarios. By the end, you will have a clear framework for deciding whether this opportunity is worth pursuing and what price level makes it attractive.

Business Overview: What Does This Company Actually Do?

Meta solves a specific problem that’s half the size of humanity, which is that advertisers can’t reach humans at scale through any other medium with the same precision and proof of delivery, operating a large social media ecosystem integrated by Facebook, Instagram, WhatsApp and Threads, giving it access to over 3.5 billion users daily in the digital era where we simply can’t put our phones down. With almost half of the world’s population using one of the platforms at least once per day, trillions and trillions worth of data points enter Meta’s servers, allowing the company to possess precise information on what you like, share, search, buy, and interact with, enabling to sell advertising to highly specific audiences. This makes Meta ads extremely valuable compared to traditional advertising.

The most valuable asset Meta owns is data, collected over two decades of user behavior, where advertisers pay to reach these users through targeted ads based on demographics, interests, behavior, and connections, custom audiences (retargeting website visitors/CRM lists, Lookalike Audiences (finding new users similar to existing customers), and AI-driven tools like Advantage+ that automate the process by analyzing user signals. Paid ads are delivered in multiple formats, across Feed, Stories, Reels, Marketplace, and Messenger, operating in a performance-driven model where advertisers bid for impressions (every time a user watches an ad), and pricing is based on cost-per-click, cost-per-impression and other engagement metrics. Once the advertiser turns the ads on, Meta starts optimizing the target audience for the ICP, with the algorithm learning as time goes by and more users interact with the ads or make the intended action, for example placing an order on an e-commerce store. When it has enough data to show the content to the right users and deliver consistent results for the advertiser, the switching costs become too high to switch to another platform and having to spend time and money again for the algorithm to optimize for the right audience, creating a moat.

Meta generates revenue in two segments, Family of Apps (FoA) and Reality Labs (RL). The first is responsible for ~97% of total revenues, making the company highly dependent on the ads segment, which is being improved with AI targeting. Reality Labs is a long-term initiative that still loses billions annually, a segment exploring AI and hardware for AR/VR, such as the Ray-Ban Meta glasses that are showing strong traction on bringing AI to the physical world and items that we use on our day to day. Meta is also closing partnerships with Oakley to make sports glasses, bringing the benefits of AI through voice commands for hands-free control, and to our daily lives outside the screens. This presents an important growth avenue that I expect to see materializing into the 2030s.

The “Free Product” Flywheel

Meta’s Family of Apps are free to use, which drives massive user growth with an algorithm that keeps showing people the content they like and share with friends. More users leads to more data, better ad targeting, higher ad prices, more advertisers interested in investing in the platform, and ultimately more users, a self-reinforcing loop that’s the engine of the business. Now imagine this with billions of users every day for many years, and near-zero marginal costs per new person that enters the flywheel.

Meta currently trades at a forward p/e ratio of 21.13, only with Microsoft lower in the Mag-7 group. Mr. Market is stressed by the $115B-$135B CapEx guidance for 2026, as if the company would need to issue stock, diluting shareholders, or taking massive amounts of debt, destabilizing the balance sheet, to support the investment cycle. The reality is that Meta generates most of its revenue through the core digital advertising business that remains a “cash machine”, maintaining gross profit margins consistently above 80%, and a balance sheet in a position of strength with more than $80B in cash and short-term investments, more than enough to invest for growth. And planning to do all of this with a positive FCF, even if lower than in previous phases with lower capital intensity, supporting a sub-optimal FCF for some time is the price we pay for a company that’s building the future.

Meta isn’t a social media company, it’s the world’s most precise human attention marketplace, operating in a duopoly with Alphabet. Together, these two companies account for almost half of the digital advertising market.

What makes this model extraordinary isn’t the advertising itself, it’s that Meta owns the attention layer of daily human life for half the world’s population, and that attention becomes more valuable, not less, every time the platform collects an additional data point. To put the advertising segment in perspective, in 2025 it generated $196.175B in revenue and $83.276B in operating income, a 42% operating margin. Despite other ventures that had gone wrong, such as the Metaverse, which we’ll get into in the next sections, the core business that’s always been advertising, keeps printing cash and allows reinvestment for growth in other segments.

Competitive Landscape & Industry

Before starting to take a look at the competitive space Meta operates in, we need to acknowledge that the company sits at the intersection of multiple tightly linked markets, so let’s break them by pieces:

Social media platforms

Meta’s whole Family of Apps is inside this category, it includes Instagram, Facebook, WhatsApp, Messenger and Threads. Social media doesn’t directly generate revenue by itself; instead, it relies on making the platforms engaging and using algorithms to keep people entering on them multiple times per day by showing the content they want to see. From the ability to generate constant attention, Meta sells advertising and rents our eyeballs to companies or individuals that want it.

Digital advertising

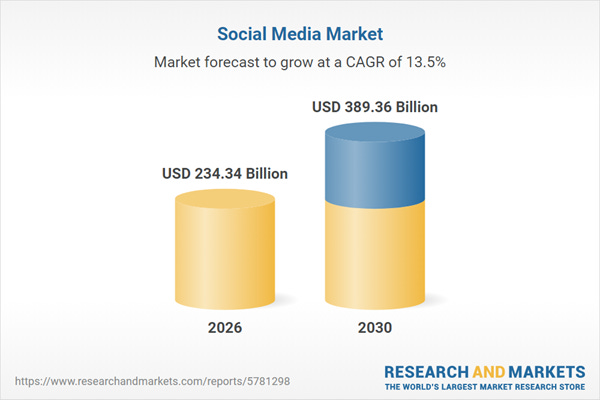

Digital advertising is the core revenue driver for Meta, a market that owns itself and is a consequence of successfully retaining people on social media platforms, benefiting from structural tailwinds such as mobile usage growth, e-commerce expansion and the shift from traditional media to digital content. This market is expected to post a solid CAGR from 2026 to 2030, of 13.5%.

AR/VR

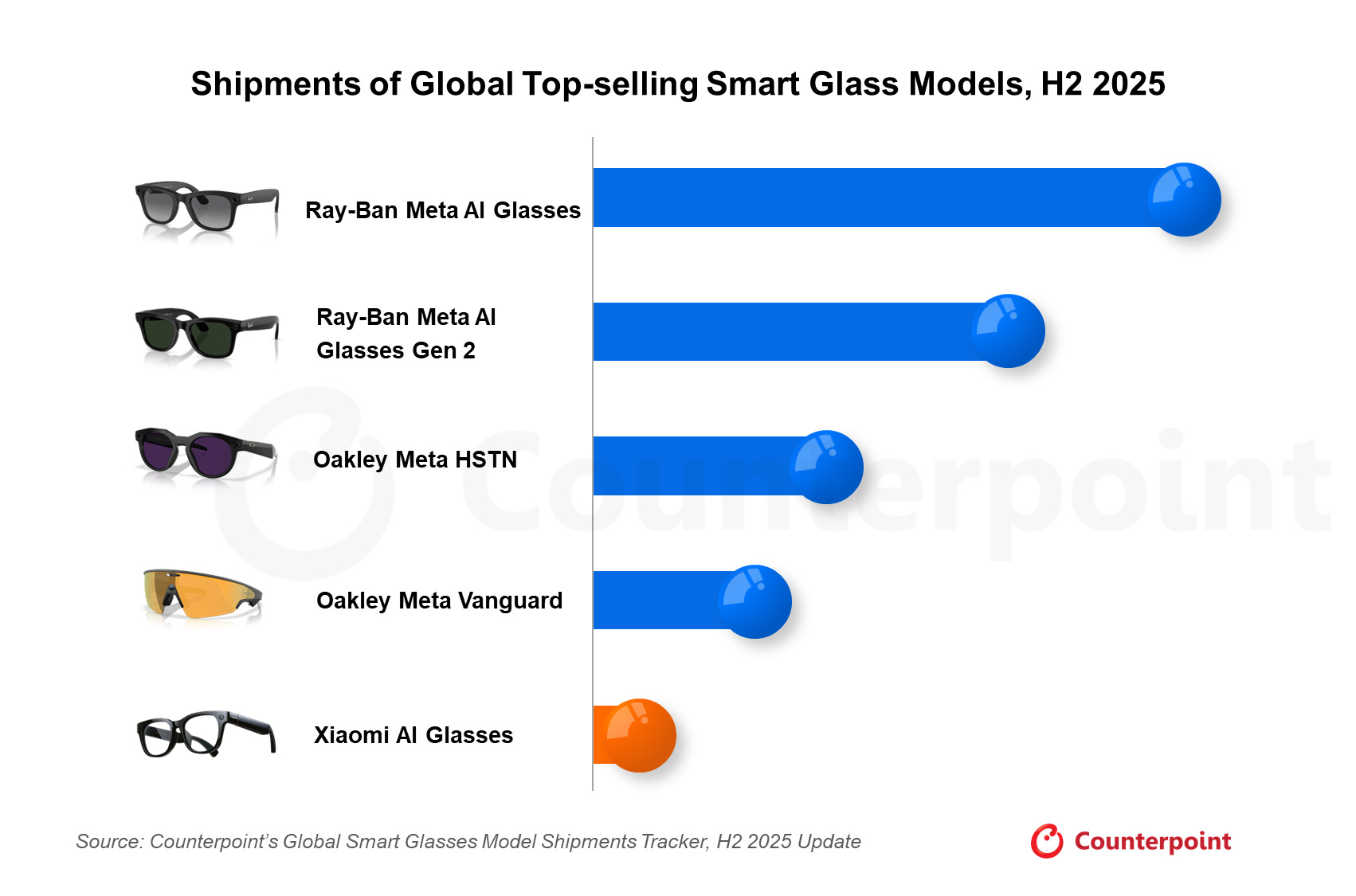

The AR/VR market has been gaining traction since the COVID-19 pandemic, and is now expected to hit a market volume of $13.7B in the U.S. this year, with a projection to reach 3.8B users just 4 years from now, in 2030, according to Statista. AR allows users to overlay digital content onto the real world, providing an interactive experience, while VR creates a complete digital environment that users can explore. These technologies are applied in multiple verticals, such as enterprise training, healthcare, retail, gaming, smart glasses, and other products that companies are building to embed AI in our daily lives. Meta takes advantage of this market through the Meta Quest VR headset line, Ray-Ban Meta smart glasses and the Oakley Meta smart glasses that catch the sports segment. Through partnerships with multiple brands, Prada is currently a rumor, Meta rapidly captures their market share, a strategy that’s proven successful with the smart glasses market growing 139% YoY in H2 2025, driven by the integration of Meta AI, allowing users to ask questions and receive answers in real-time. Meta is basically alone in the global smart glasses market as of H2 2025, with a commanding 82% share and a massive adoption, over 7 million Ray-Ban Meta glasses were sold in 2025, more than triple the combined sales of 2023 and 2024. I strongly believe that the growth of this segment in the next few years is what will turn Reality Labs into profitable territory after the Metaverse disaster.

TAM, Growth Rate & Key Structural Trends

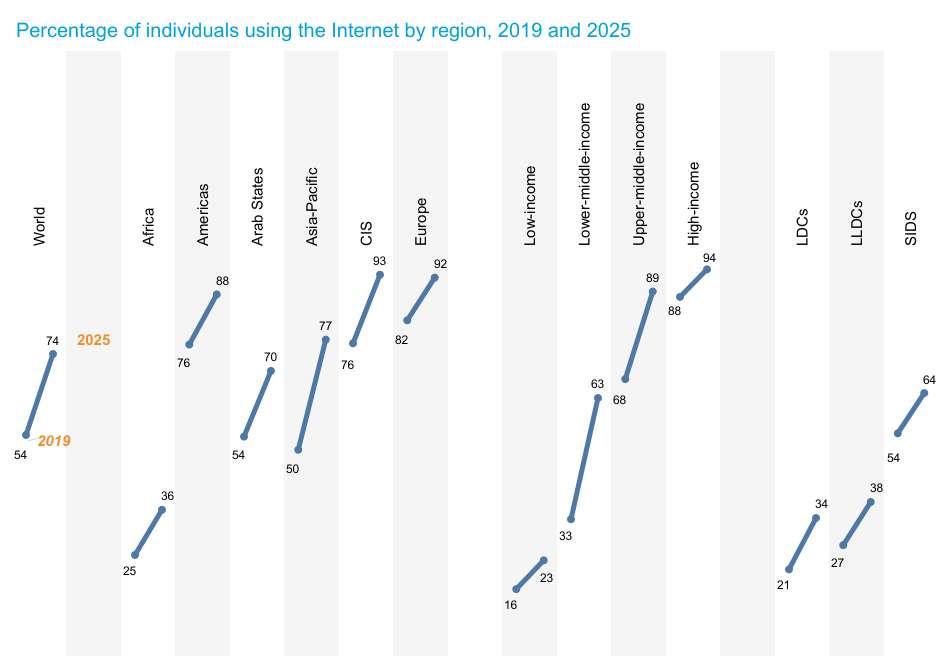

Meta’s Total Addressable Market is vast, covering the global digital advertising market that includes paid media shown in social media platforms and emerging AI opportunities, serving roughly 8 billion potential users. As of early 2026, over 6 billion people are using the Internet worldwide, which indicates a trillion-dollar TAM, and that explains why Meta deserves a trillion-dollar valuation. As the company already does a pretty good job retaining people on its platforms, so good that some courts are considering it to be addictive, something we’ll analyze in the Risks section, there are major growth opportunities in emerging economies that are rapidly progressing, and as the purchasing power of their populations becomes higher, it will eventually lead to more businesses using Meta Ads to drive sales to their products and services.

According to ITU, high-income countries are nearing universal Internet usage, with 94 percent of the population using it. Even though, only 23% of the population in low-income countries is using the Internet. Europe and the Americas are leading with between 88% and 93% of the population already using the Internet, while Asia-Pacific and the Arab States regions are still at 77% and 70%, respectively. Africa is just at 36%. If in the next decade the Asia-Pacific and the Arab States regions reach the same levels of Europe and the Americas, with a combined population of around 5.3 billion people, we can project a revenue increase in the dozens to a hundred billion dollars to Meta’s income statement, considering the ARPU of $57.03 registered in FY2025. This takes into account that almost everyone that uses the Internet ultimately starts being active in some of the platforms offered by Meta, which we can assume as of today.

With AI improving ad targeting, there’s no reason to be pessimistic on the future growth of the core business, advertisement.

Competition

Despite owning market-leading positions, Meta faces other giant rivals that compete for user attention and advertisers’ budgets. Understanding the angles of these key players is crucial for a comprehensive analysis of the position Meta occupies in the market, so let’s start by analyzing them one by one:

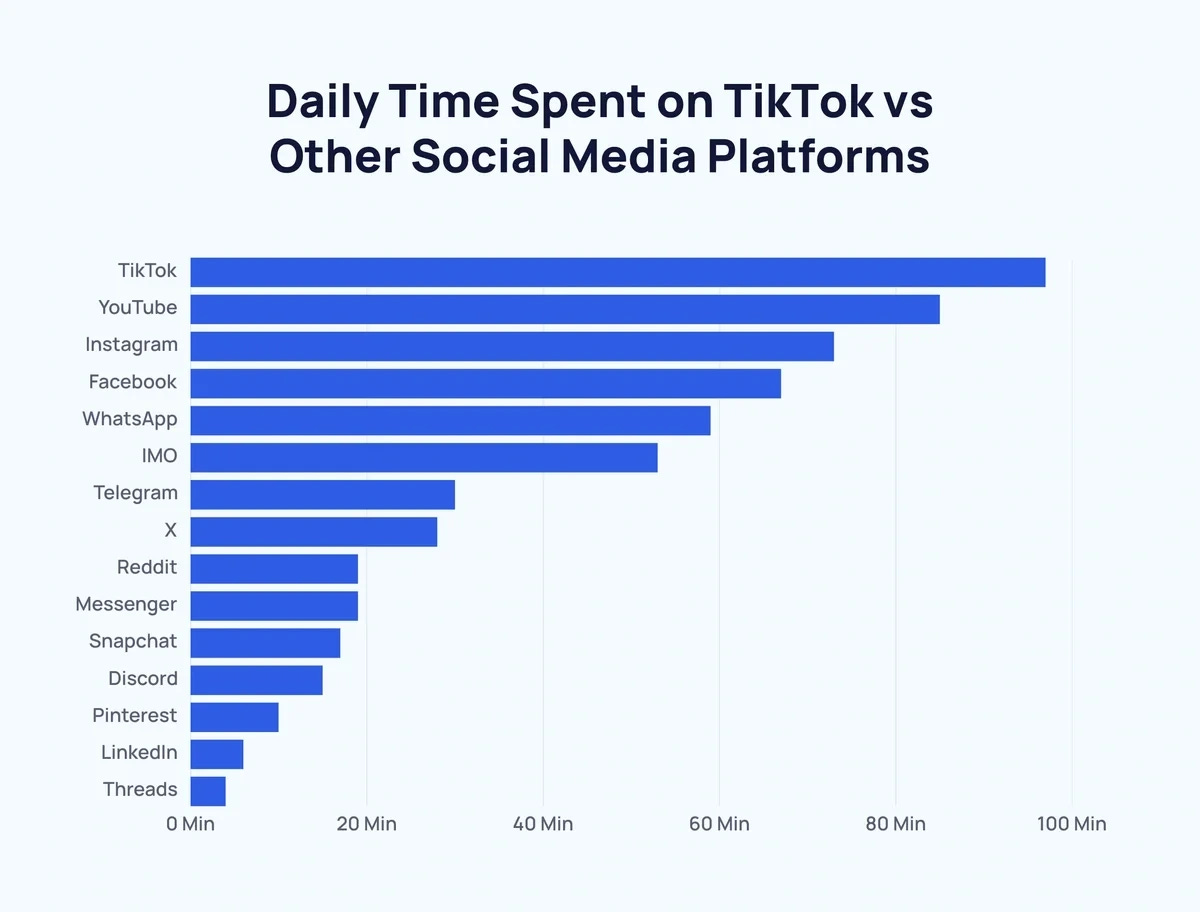

TikTok (ByteDance): TikTok is a significant competitor in the current short-form content trend that drives the highest engagement, boasting an impressive 1.9 to 2 billion monthly active users worldwide. Meta is competing for these same users with Instagram Reels, also with 2 billion monthly active users that generate 140 billion daily views, so we can assume that the company is doing a good job at not losing market share against TikTok.

Google (Alphabet) remains the world’s largest advertising company, an undisputed leader in a market that’s not directly related to Meta’s one, the search business. On the video side, YouTube accounted for roughly 15% of the social media ad spend.

Snapchat is another key player in the social media space that competes for much of the same younger demographics as Meta, offering unique augmented reality features that raise security standards by showing videos that can only be watched during a short period of time before being eliminated, although the company has a much smaller scale with just roughly 2.5% of the global social media ad spend in 2025.

Pinterest differentiates itself through its visual discovery platform targeted specifically at users seeking inspiration and product ideas, also a minor player with less than 2% of the global social media ad spend.

Meta has a competitive edge against its rivals, the most direct one being TikTok because it wants many of the same users. None of the other companies benefits from the extensive network effect across the Family of Apps. The combined user base of Facebook, Instagram, and WhatsApp creates a powerful network effect, where each new user enhances the platform’s value for the other, improving and benefiting from AI initiatives trained on a two decade data flywheel that poses a high barrier to entry for new competitors.

The company’s sophisticated advertising technology enables it to generate most of the revenue through highly targeted ad placements. AI-powered ad tools and algorithms allow personalized content and an optimized performance. Advantage+ Shopping Campaigns have shown a 15-30% improvement in ROAS over the last year. Improvements in the AI recommendation systems led to a 5-7% increase in time spent in Meta’s core platforms, Facebook and Instagram. This world-class performance explains why Meta captures a substantial portion of social media ad spending, reaching 60-65% in 2025.

On the most recent initiative that’s been buzzing, the smart glasses market, Meta dominates it with an 80% share as of late 2025. The approach of doing partnerships with well-know glasses brands as been proving to be a successful decision, it enables to combine customers of both companies and instantly capture market share, now expanding to the sports segment with Oakley, the Oakley Meta HSTN and Oakley Meta Vanguard, together accounted for over 30% of Meta’s total shipments in Q4 2025. I expect this market approach to continue being fruitful as more and more people look for wearables that integrate AI into their daily lives. The global AI wearables market is projected to grow at a 21.3% CAGR for the period between 2025 and 2035, according to Prudence Research.

Competitive Moat

We’ve already touched on many points that make Meta’s wide moat, but it’s important to go a bit deeper. Meta’s moat is made of multiple layers, including network effects on user distribution, advertiser ecosystem that locks demand, data and AI feedback loops that improve ad targeting and ROAS over time, creating high switching costs after the algorithms learned what brings results, a multi-app portfolio of the top 3 social platforms, and infrastructure investments that only a handful of companies in the world have the resources to do.

Social media networks are winner-take-most markets, where growth scales nonlinearly with users and new entrants face the cold-start problem of getting the ball rolling. No other company has the moat of owning the daily attention of half the world’s population. The mechanism is pretty straightforward, users attract content creators, these attract businesses buying advertising, and businesses attract more users. WhatsApp adds a retention layer for people that get into Meta’s ecosystem without looking for entertainment.

Advertising is the economic engine behind all the work Meta puts at retaining users on the Family of Apps. Growth for the next few years will be driven by AI tools (Advantage+) and short-form content like Reels. Advertisers choose Meta Ads because of the global scale, strong ROI due to targeting and optimization, and an integrated funnel that goes from discovery to conversion. Algorithms are improved the more users adopt it, which leads to better ads, more advertisers, better results, and more investment in the product.

Another layer of the moat, and one that no other company can dethrone, are the trillions of data points that live inside Meta’s servers and were collected daily for many years. All these interactions are now fed into AI-enhanced personalization to generate high-quality behavioral data. AI improves ad targeting, content recommendations, and feed ranking. This creates a self-reinforcing loop where more usage leads to more data, better AI, more engagement, and more usage. This a key distinction for TikTok, the company is much more recent that Meta and doesn’t benefit from all the data accumulated through decades.

Family of Apps allows Meta to avoid relying on just one platform and owning just one specific demographic. Facebook is the oldest one that continues having a global reach but tends to be used by older generations, as Instagram is more visual, and allows for a rapid consumption of content that captures the younger demographics’s attention. Messenger is just an utility layer and WhatsApp is also by the professional segment through the Business vertical. Meta Ads determine which platform is the most effective to show the ads that businesses paid for, owning a shared ad infrastructure is something that no other competitor can rival with. Competitors typically have one strong app; Meta has an ecosystem.

It’s important to mention certain points where the moat is more fragile than it appears. One is that user switching costs have never been lower and people shift attention between multiple platforms that come out of Meta’s Family of Apps, such as Youtube and TikTok, there is no hard lock-in like in enterprise software where contracts are signed for multiple years and retention is guaranteed that way. TikTok showed us that disruption is possible, and they did it through algorithm-first short-form content that forced Meta to quickly adapt and launch Reels, so we can see that moats are in constant mutation and there’s no space for getting complacent. Third-party platform dependence is a structural weakness vs Google, iOS privacy changes already damaged ad targeting, and advertisers’ budgets shifted away from Meta, not owning the distribution rails can bring some unexpected surprises.

Management Assessment

Meta’s leadership is still the responsibility of Mark Zuckerberg, the 41-year old CEO that founded the company at 19 in the Harvard dorm room. Founder-led companies tend to outperform the rest of the market due to mission-driven ownership, long-term orientation, and willingness to take asymmetric bets. Although, there is also the downside, such as the key-man risk that Meta publicly acknowledges in the 10-K report.

In terms of skin-in-the-game, Mr. Zuckerberg clearly has it, he owns 99% of Class B shares, roughly 14% of company’s equity, and more than 60% of the voting power, ensuring controlling interest. Meta stock ownership is basically his entire net worth, if we invest in the stock and the company goes under, he goes with us.

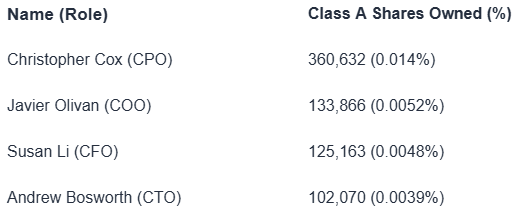

Now evaluating the stock compensation weight on other members of the c-suite from the latest DEF 14A proxy statement, we can see that executives’ compensation is explicitly designed to be equity-heavy, with 60% allocated to PSUs and 40% to RSUs. A typical Meta executive pay structure is composed of base salary, bonus, and equity awards (PSUs + RSUs). Equity compensation is the majority of total pay (often 70-90%), and cash (salary + bonus) is the minority. Meta states that it chooses equity as the primary incentive vehicle tied to long-term performance. Nonetheless, we need to acknowledge that executives own very little stock outright, most of their exposure are Unvested RSUs, regularly sold after vesting, so the retained ownership is low.

The value of the Class A Shares owned by the executive team is in the multiple 8-figures territory, so for people with their profile we can safely assume that Meta stock occupies the vast majority of their net worth. There’s no doubt that their incentives are aligned with ours.

Management Track Record

Mr. Zuckerberg controls the majority of the company, the board can’t overrule him, and shareholders can’t exercise influence, while also being CEO and chairman, so short-term and strategic decisions are centralized on him. Despite this, Zuck has repeatedly demonstrated correct long-term platform calls with multiple major wins, otherwise Meta wouldn’t be one of the largest companies in the world. We can reference some of those wins, such as:

Pivot to mobile (2012–2014)

Acquisition of Instagram (2012) for $1B, now valued at $200B–$500B range

Acquisition of WhatsApp (2014), 450M users on that date, and no 2B+

Shift to short-form video (Reels vs TikTok)

AI-driven feed (moving beyond social graph)

All of these decisions proved successful, especially the acquisitions of Instagram and WhatsApp, both companies entered in the Family of Apps, the flywheel that today generates almost all of the revenue, and therefore created enormous value for shareholders since then.

In terms of capital allocation, Zuckerberg behaves more like a venture capitalist inside a mega-cap company than the typical Fortune 500 CEO. His style are asymmetric, high-conviction bets, willing to deploy tens of billions of dollars into uncertain initiatives like Reality Labs, initially investing on metaverse and now pivoting to AI wearables, and looks like this segment might be getting closer to finding its way into profitability. Now the AI CapEx ramp up is in line with what the other mag-7 executives are doing. Above all, this CEO is a product-thinker at scale.

Capital Allocation

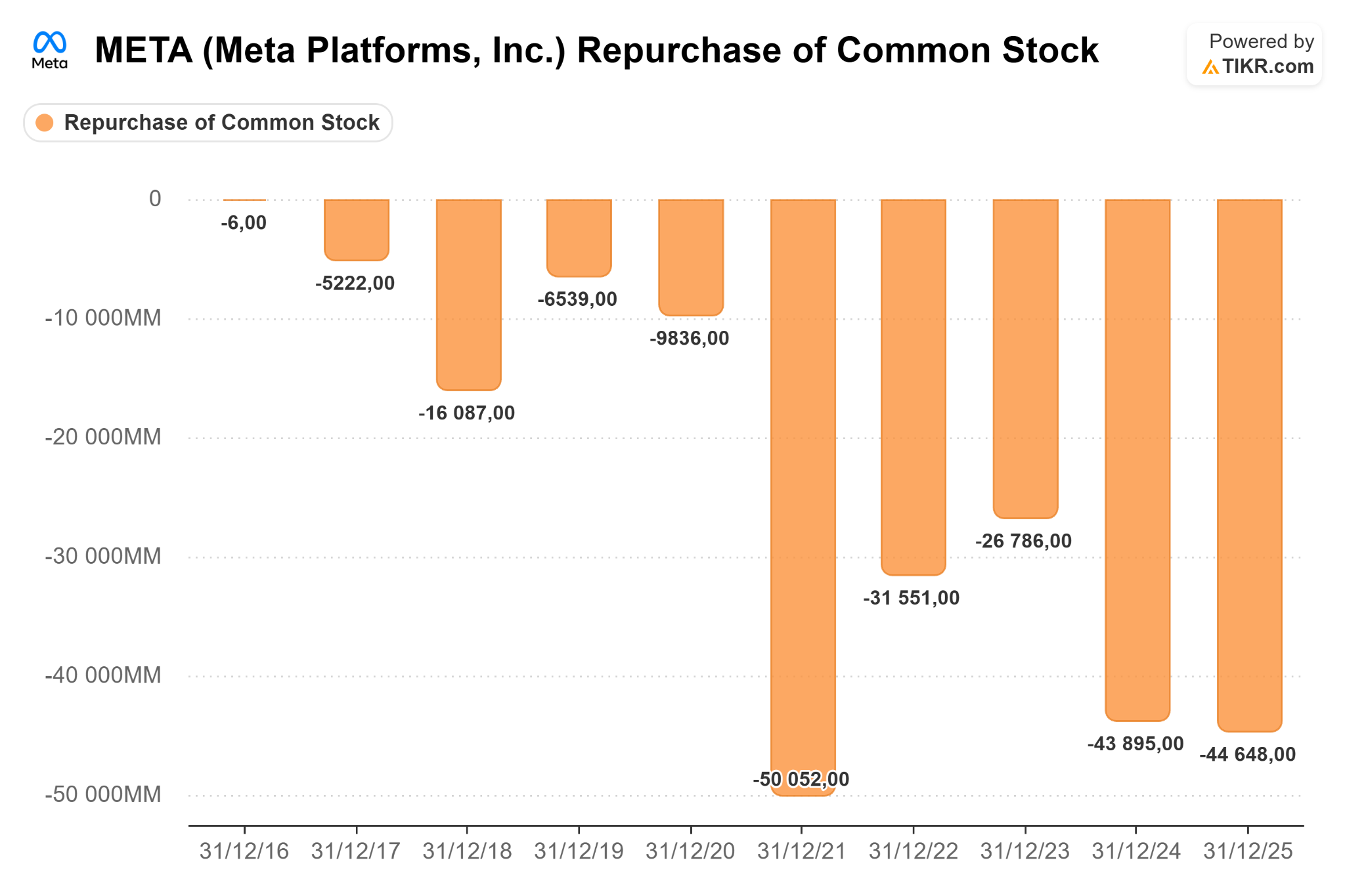

Let’s take a direct look at where free cash flow has been deployed, and how much of it was returned to shareholders through buybacks and dividends.

We can see unusually strong buybacks in 2021 due to peak cash flow and limited reinvestment needs compared with today. Post-2021, buybacks became inconsistent because capital redirected to AI + Reality labs, and earnings were temporarily depressed due to losses in the failed metaverse venture. In 2021, AI infrastructure spending hadn’t exploded yet, Reality labs wasn’t at peak burn, and no major platform required urgent spending, so as there was nothing better to do with it cash, buybacks were an option when the stock was trading at 20-25x earnings (reasonable for growth).

From 2022-2023 until now, privacy changes from Apple reduced ad targeting efficiency, leading to lower margins and a less predictable cash flow. The AI arms race has also been a capital sink, the massive investment in GPUs, data centers, and models, lights a competition between buybacks and investing for growth, management has consistently preferred the second one. Compared to other big techs, Meta doesn’t treat buybacks as fixed policy, instead, Zuckerberg uses them as residual capital allocation. Buybacks are optional and strategic investments are mandatory, Meta isn’t a capital return company, but a capital allocation one.

Financial Analysis

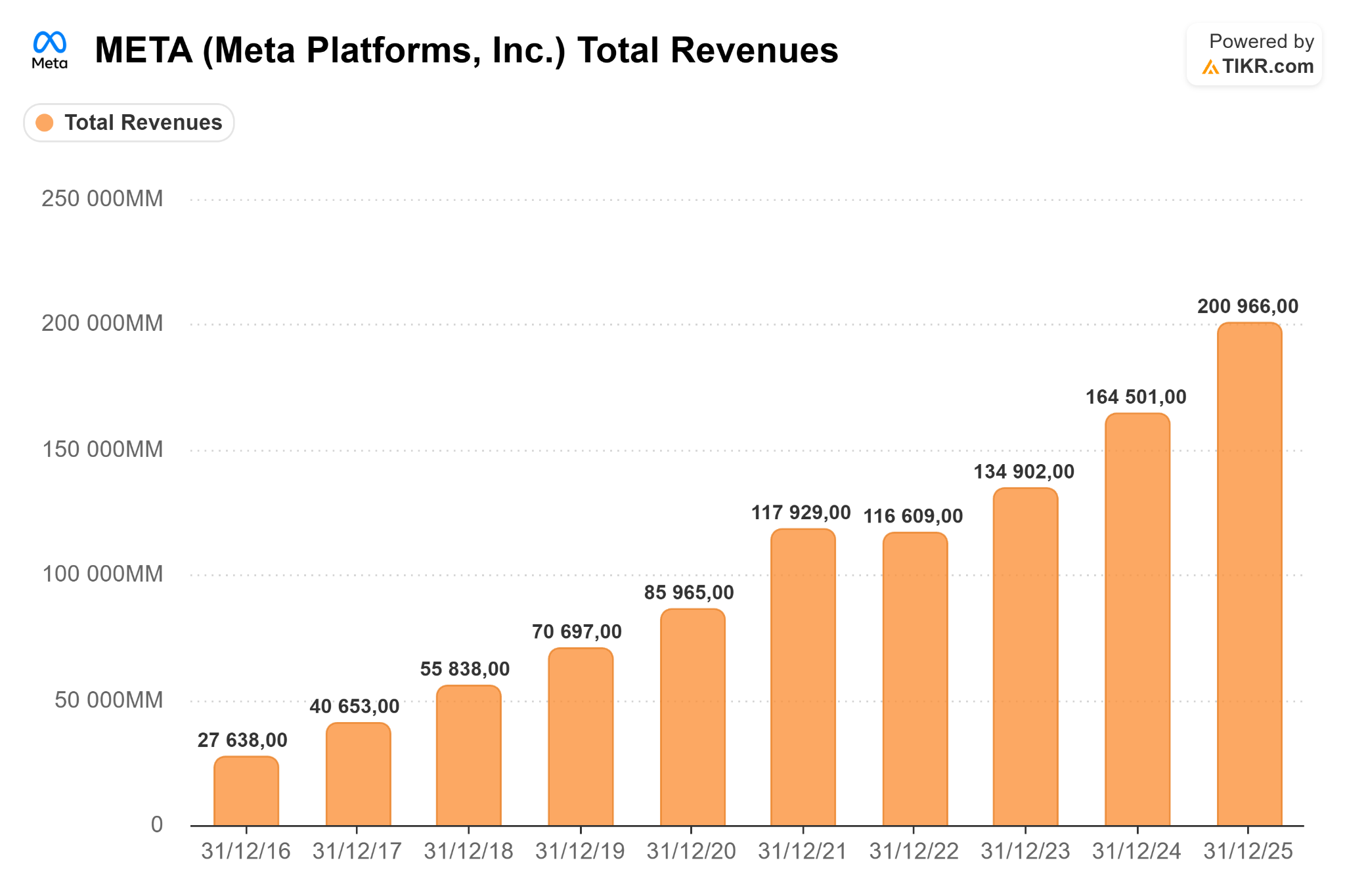

Revenue 10-year CAGR: 22%. A consistent and linear growth every year, only stagnated in 2022 after the 2021 boom.

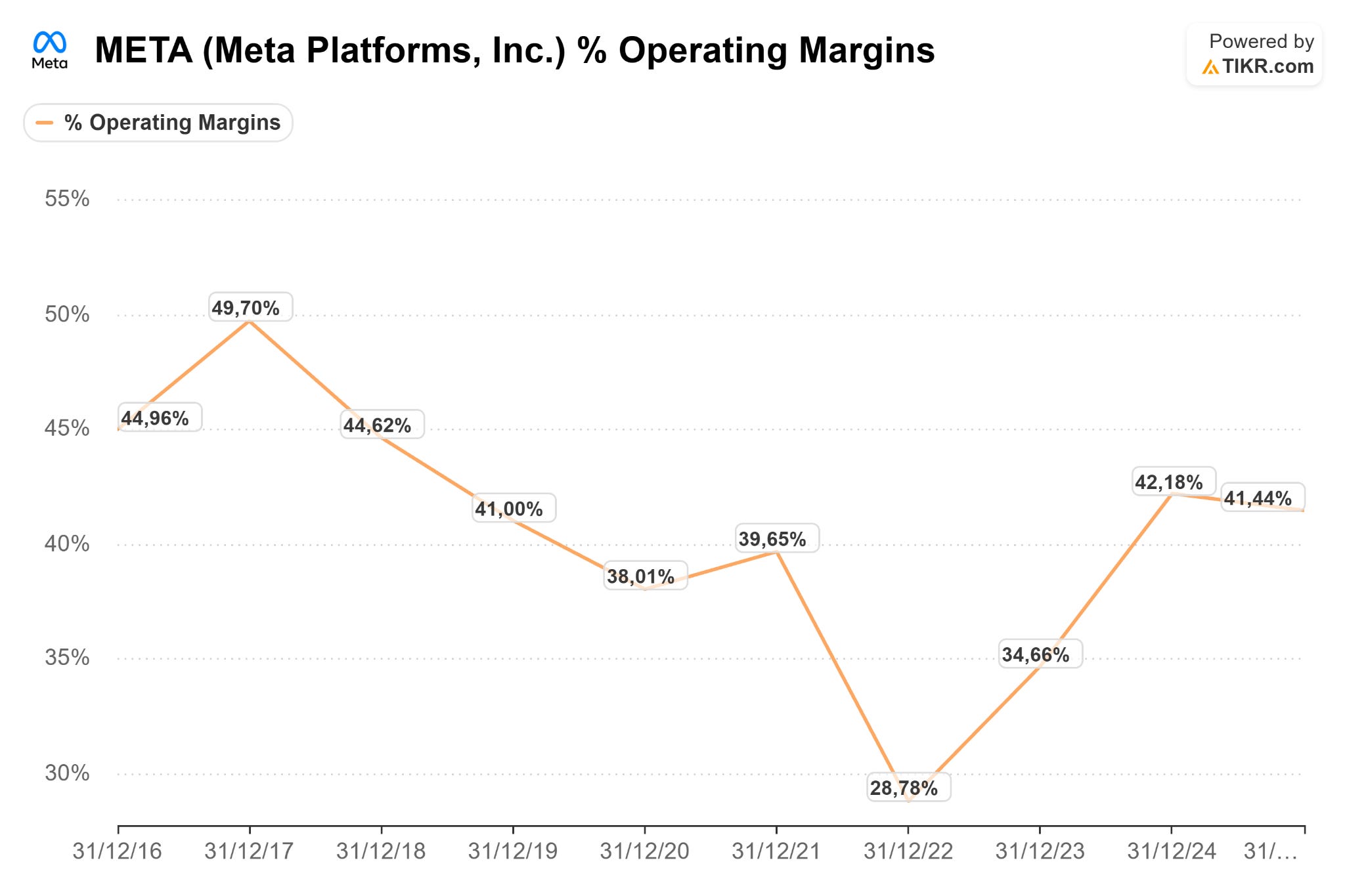

Operating Margin has been consistently in the 40s, temporarily suppressed after the Apple privacy changes and now picking up with the AI ad targeting improvements:

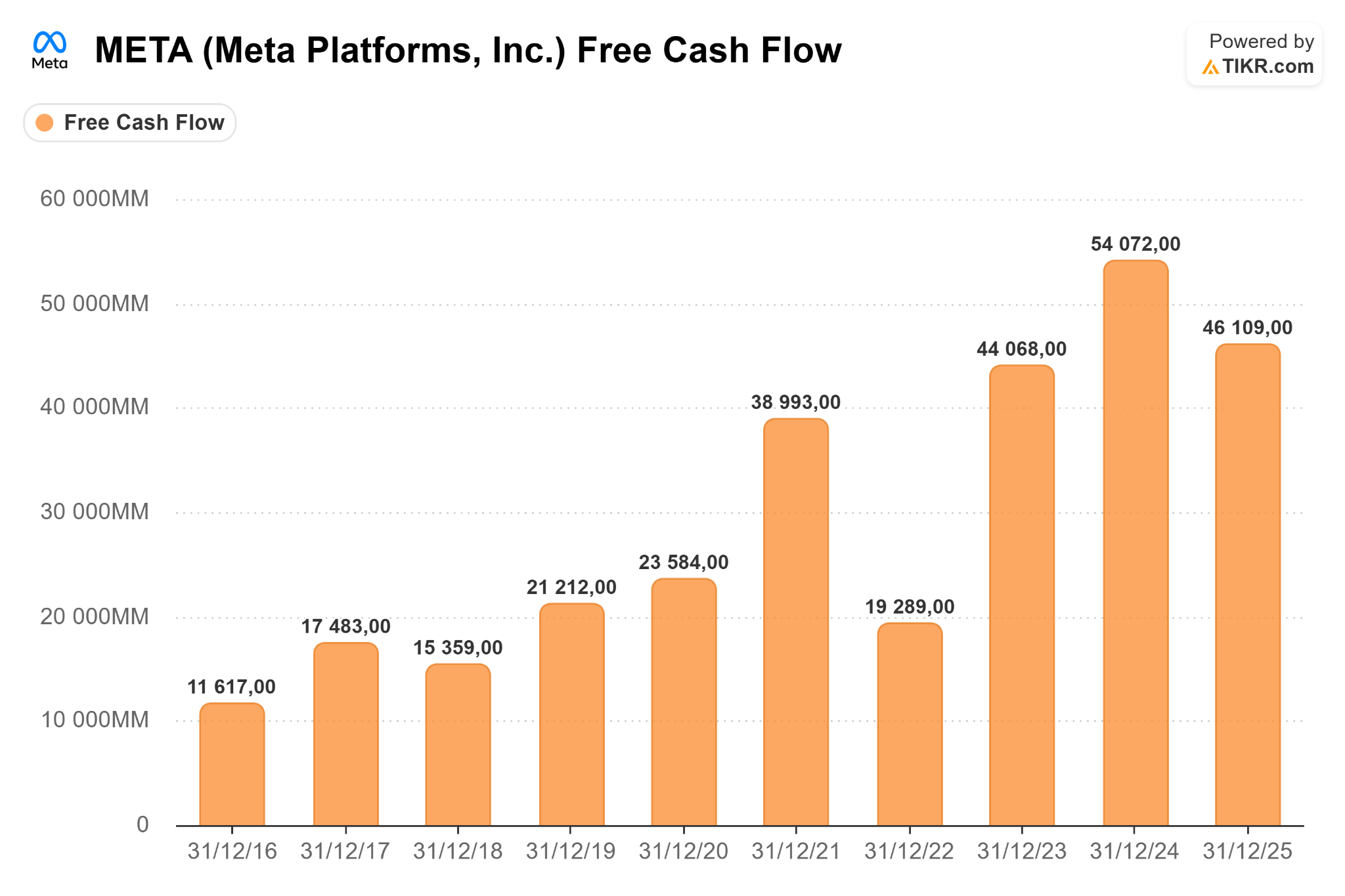

Free Cash Flow 10-year CAGR: 14.8%. Solid cash-generating capabilities, also picking up after the 2022 dip, for the same reasons:

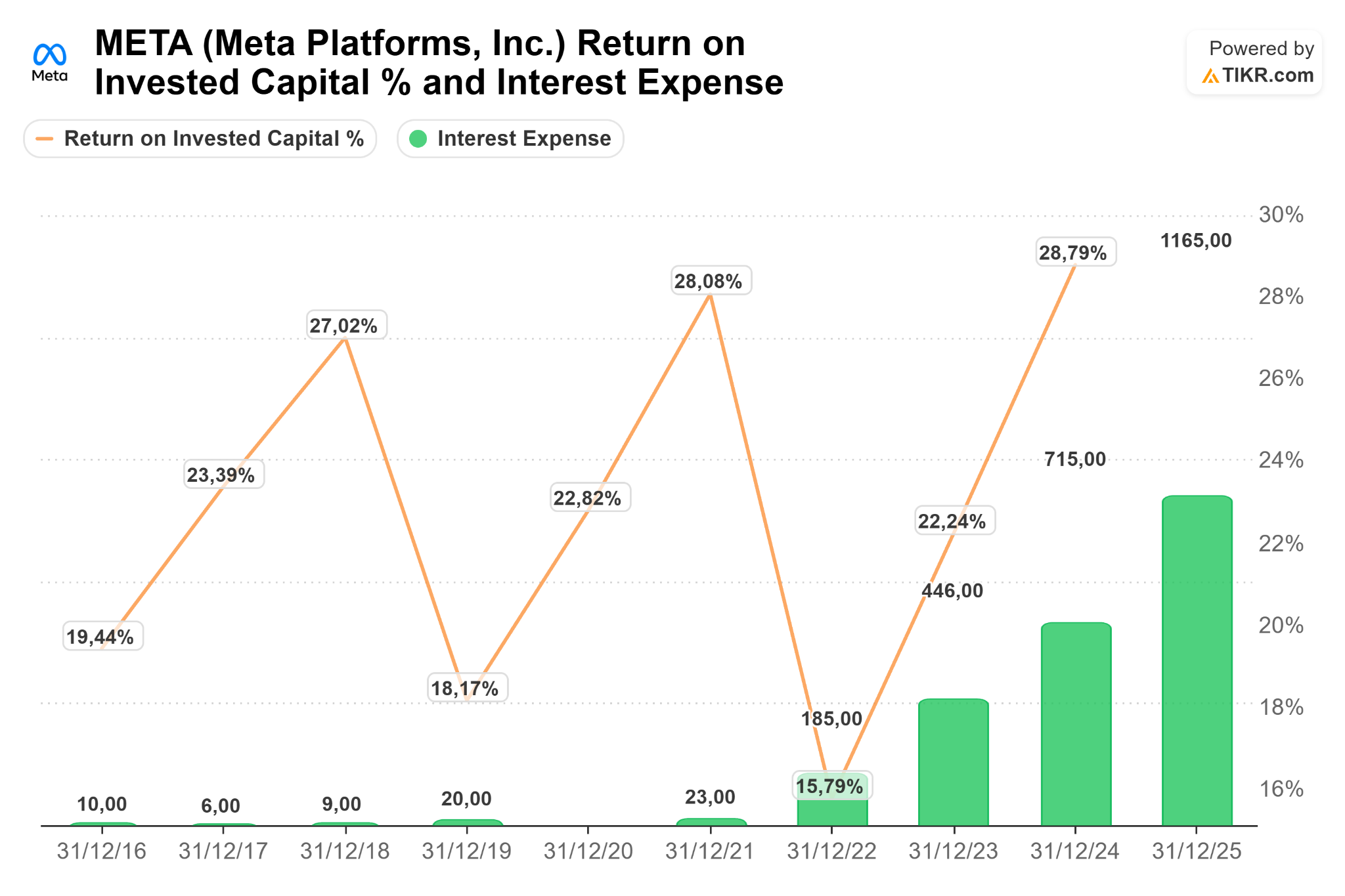

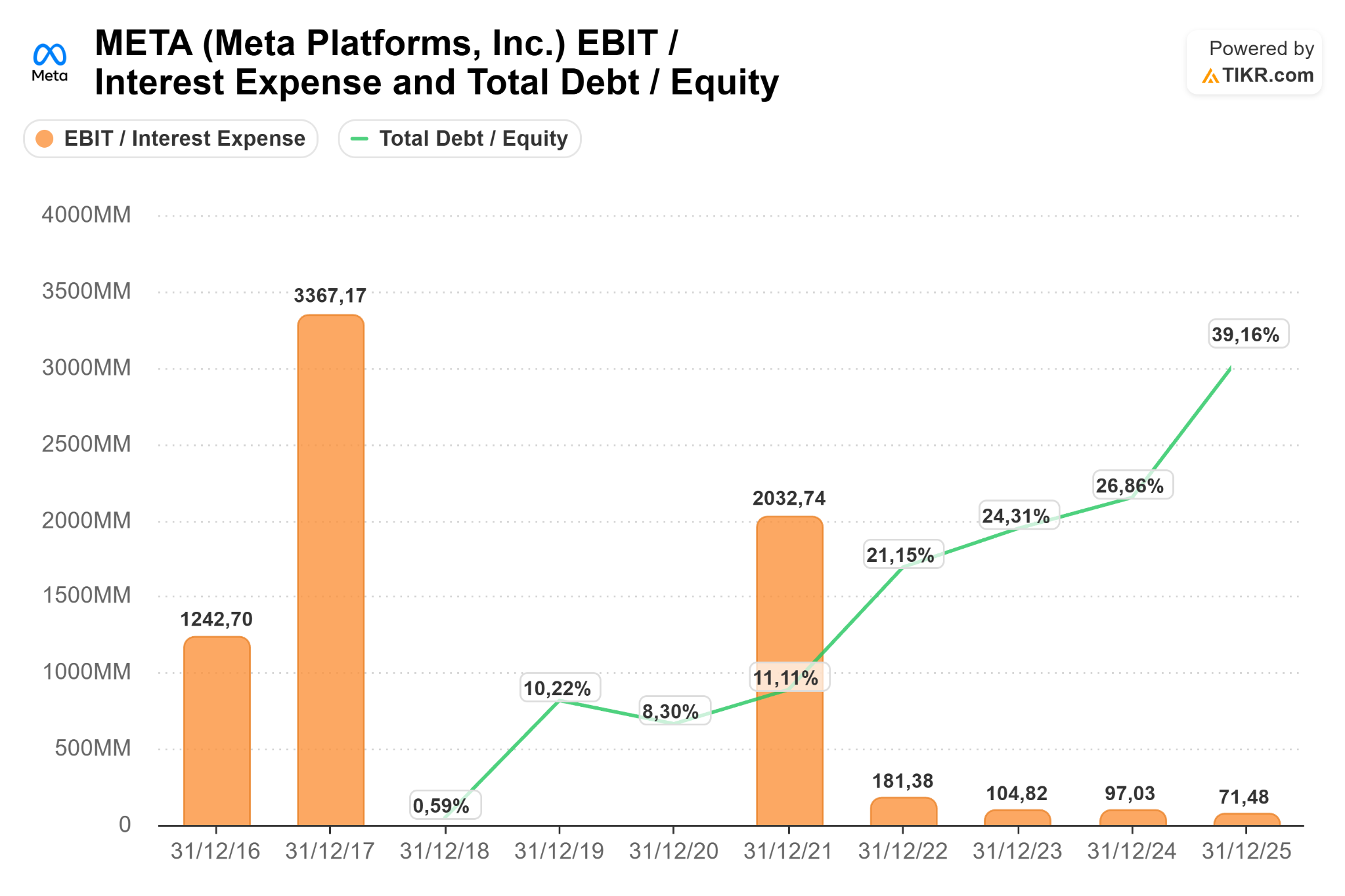

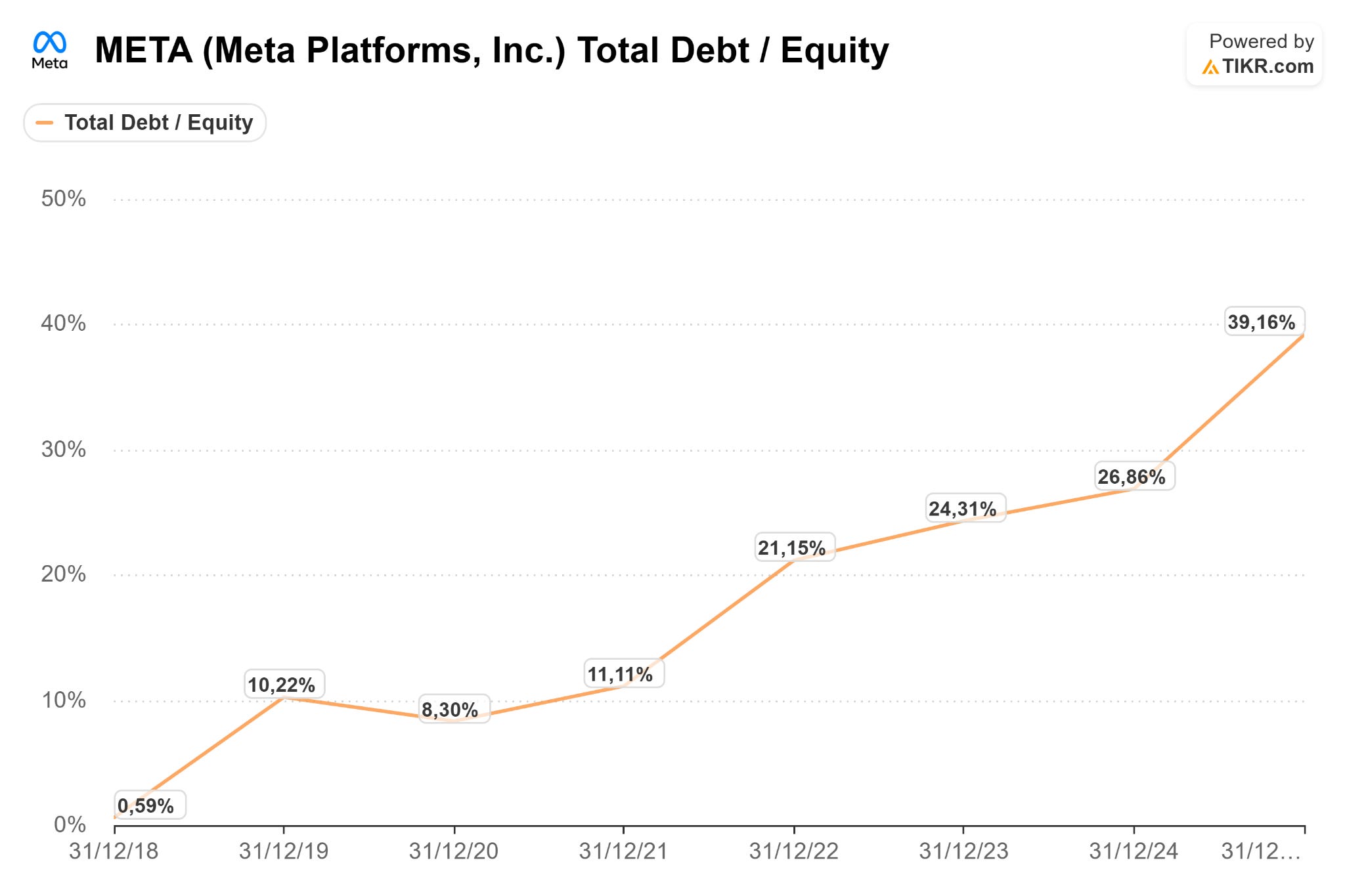

ROIC and Interest Expense shows us that Meta has been taking more debt for the current investment cycle, even with ROIC at an ATH with a healthy recovery:

Debt/Equity and EBIT/Interest Expense demonstrate a view that’s consistent with what I wrote above, debt has been increasing, if goes above 50% of equity might deserve more attention. EBIT still covers Interest Expense more than 70 times:

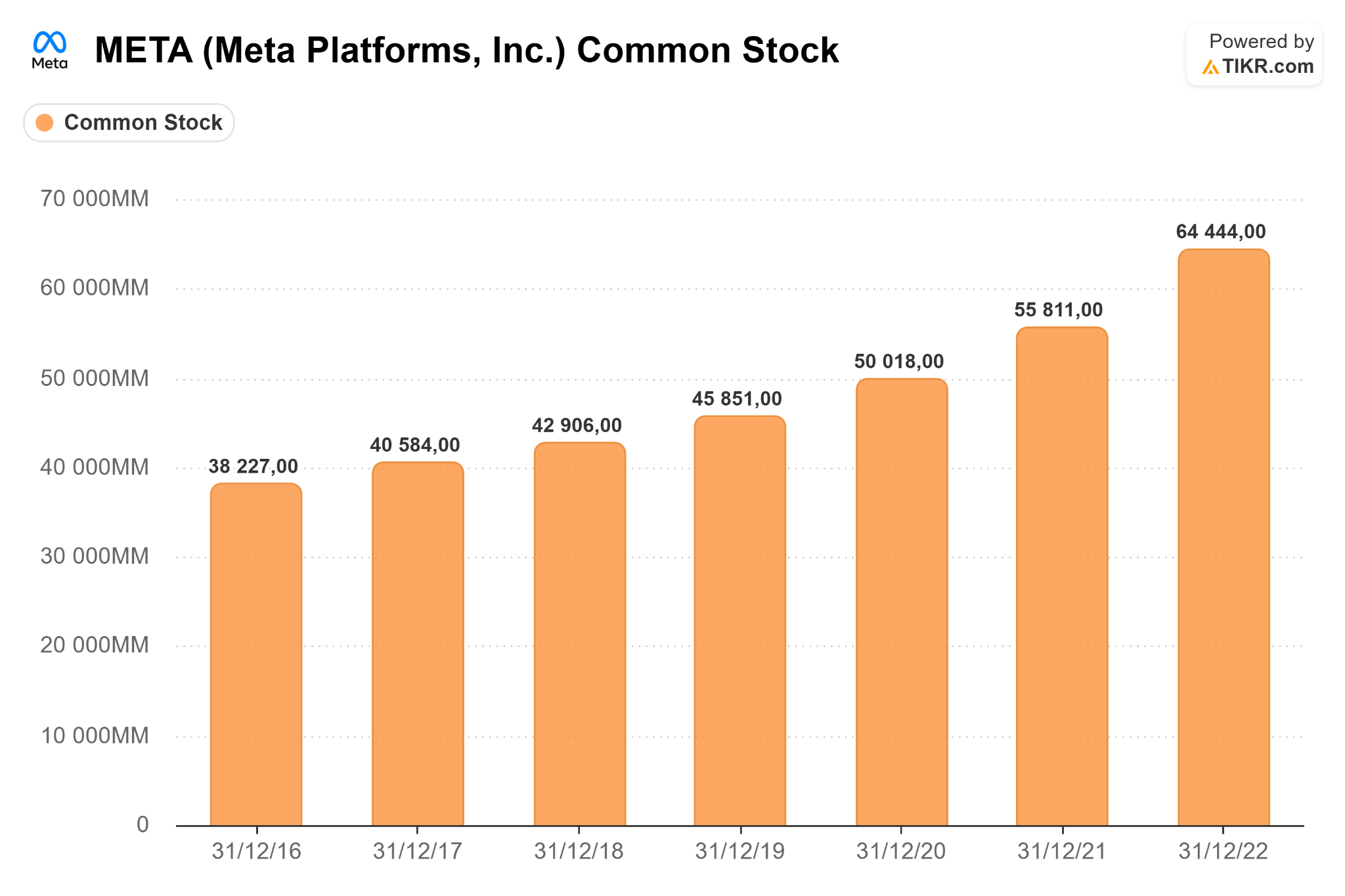

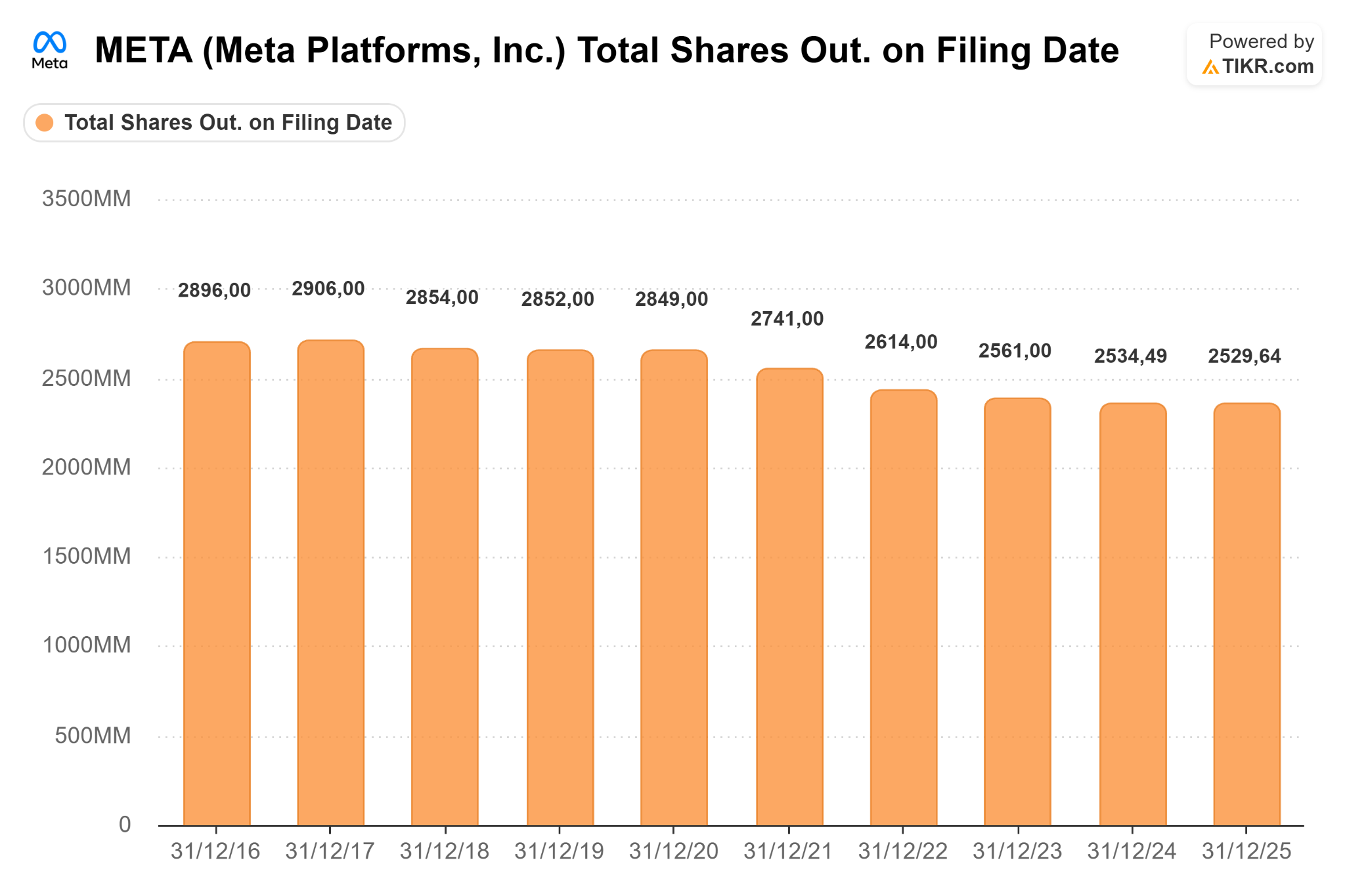

Even with data just until 2022, the common share count has been rising upwards due to the need to retain AI talents that are very expensive:

Dividend & Capital Return History

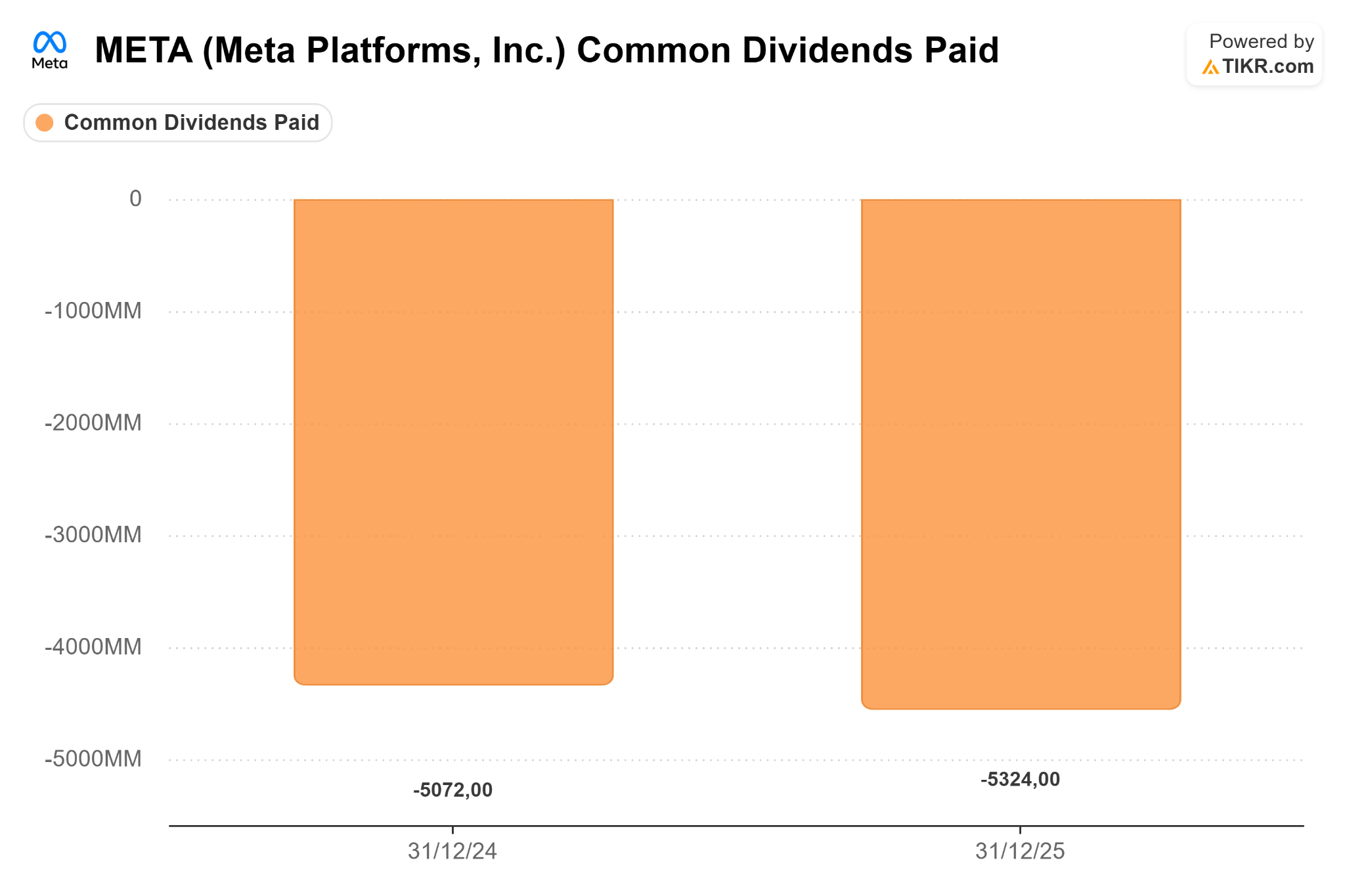

As we already analyzed buyback history, I’ll keep this shorter and just talk about dividends, and why Zuckerberg decided to take a different view in 2024 to start paying them.

Meta started paying a dividend because it crossed from “pure growth” into “cash-generating platform with surplus capital”. After 2023-2024, margins recovered after the 2022 downturn, AI improved ads efficiency, and the core business started moving up strongly. Getting into dividends also broadens the investor base for the ones that have a dividend mandate, signaling maturity and confidence in long-term cash-generation capabilities. Despite dividends still being in the early days for us to draw any conclusions, I expect them to stay small and have an inconsistent growth for the next few years, as everything tells us that the company will continue the tradition of giving up short term capital return to shareholders for long-term bets.

Growth Outlook

Despite being a trillion-dollar company, Meta still has pretty promising growth drivers for the next few years. Meta grows most of the revenue through ad impressions (volume) and price per ad (CPM). Growth is coming from better targeting via AI, which leads to improved ROI and advertisers end up paying more. So, there’s no need to chase new clients, monetizing existing ones is cheaper and better, while also creating higher switching costs. The adoption of Advantage+ automated ads has been gaining adoption and is one of the main reasons for the success at retaining advertisers’ budgets through a higher ROI.

Another huge runway are new monetization surfaces, for example WhatsApp has 3B+ users and only recently added ads/business messaging. Threads are still in early-monetization phases, and Reels are scaling revenues vs what was already achieved through Feed/Stories.

One specific point that I want to emphasize is geographic expansion. Meta already has ~3.5B daily users globally, but revenue is uneven with US/Europe at a high ARPU, and Asia/Africa at a low ARPU with a high growth potential. In Asia, the middle class is expanding rapidly, and this is a significant macro tailwind where higher smartphone penetration, internet usage, and digital payments, lead to more people creating more businesses with more advertising demand.

ARPU is much lower in Asia than in US/Europe, so the growth has to come from monetization catch-up, not just user growth. Monetization gap is wide and competition is strong, TikTok has a large presence in Asia. For the creator ecosystem to scale, and for the emerging markets to start generating meaningful cash, we are looking at a trend for the next decade. Ultimately, this can add a few dozens of billions of dollars to Meta’s revenue.

The digitalization of businesses in developed markets also presents major growth tailwinds, as more companies get into the digital world, eventually they’ll start looking for ways to promote their products or services through these tools, and Meta Ads will be there, waiting for them with AI-improved targeting.

Risks

The most important risk that’s important to acknowledge is the dependence of only one revenue model, we can say that almost all the money that Meta generates comes from the advertising segment. It’s 97% of the business relying on two things the company doesn’t fully control, user attention and third-party data signals. We’ve seen the damage that depending on external platforms can make, Apple’s iOS 14.5 App Tracking Transparency (ATT) update cost roughly $10B in revenue in 2022, drastically reducing Meta’s ability to track user behavior across apps. It limited access to Identifier for Advertisers (IDFA), ATT caused weaker ad targeting, unreliable reporting, and significantly higher costs per acquisition (CPA) for advertisers. The dramatic loss in ad targeting efficiency and conversion results, led to a dip in advertisers’ spend inside Meta Ads. To mitigate this risk, Meta started using server-side tracking (Conversion API) to feed data into the servers, not relying on browsers. Now the conversion attribution occurs in a time window that determines how long after an interaction the purchase still relates to the ad. For example:

Day 1: you see an ad on Instagram Stories but don’t click.

Day 2: you click on an ad in Facebook Feed but don’t buy.

Day 5: you see another ad on Instagram and make a purchase.

Considering the window is 7 days post-click, the conversion will be attributed to the Day 2 click, even if the purchase happened three days later.

Another way that was implemented to avoid dealing with privacy issues, is the Aggregated Event Measurement, these are protocols to manage ad campaigns that limit conversion events to eight per domain.

The last one is conversion modelling, using machine learning to estimate and fill the data gaps caused by users who opt out of tracking.

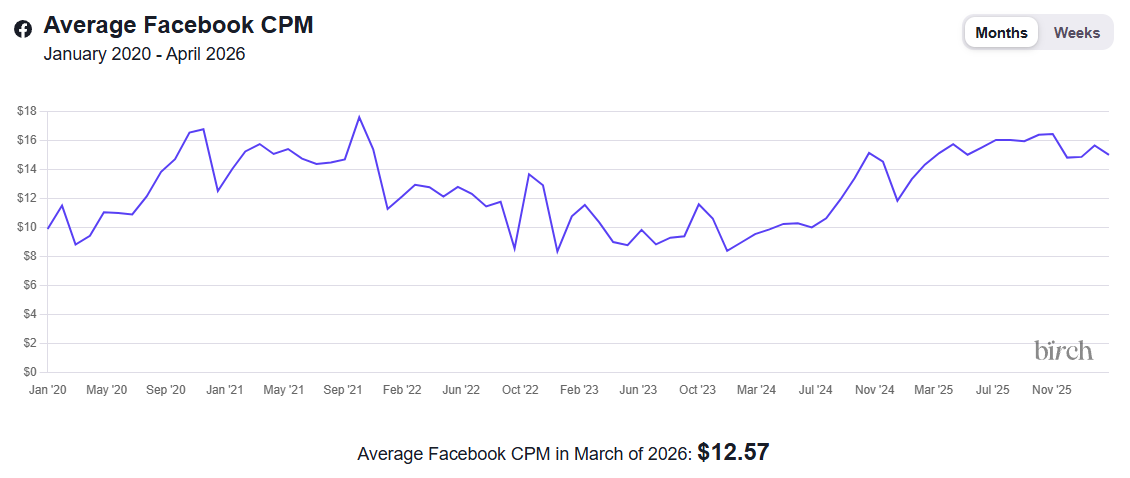

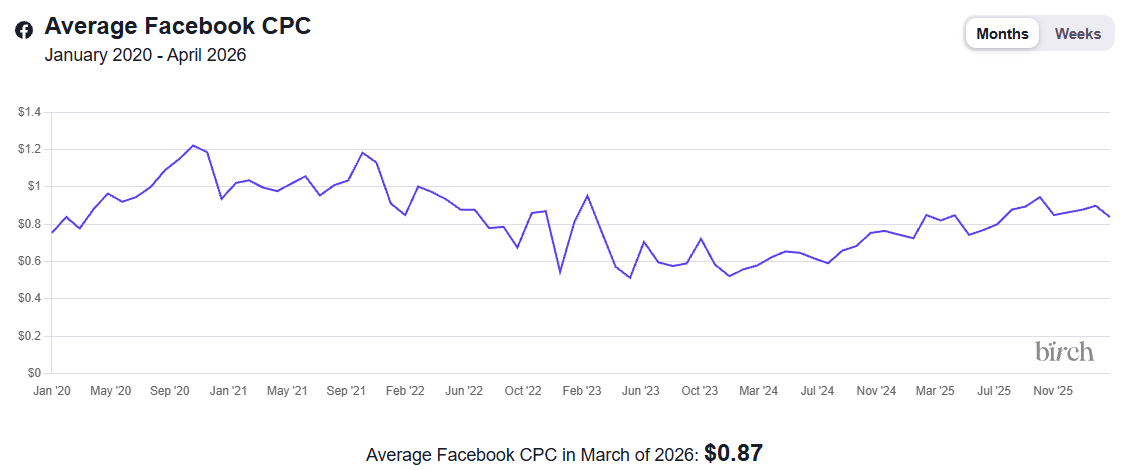

The average Meta CPC chart is consistent with the higher costs seen in 2021 and 2022 due to the iOS update, and since then it stabilized due to Meta’s measures. Advantage+ and on-platform signals helped mitigate this, but we should be aware that further OS-level privacy restrictions, or a shift in advertiser sentiment, could harm the business that has no real fallback if advertising economics deteriorate, WhatsApp monetization and Reality Labs are years away from compensating.

Competition from other companies needs to be emphasized, TikTok is a real threat in the short-form content that today dominates ad formats. Both companies, Meta through Instagram, have a reach of 2B monthly active users, but TikTok’s average daily time-on-app has consistently exceeded Instagram’s, meaning Meta might be losing on engagement intensity, which is exactly what drives CPM. If this gap widens, advertisers might notice in ROAS data and very quickly switch platforms.

Alphabet generates most of its revenue through search advertising, which isn’t the same market as Meta, although YouTube competes directly and aggressively for the same video ad budgets, which already brought in more than $40B in FY2025. Connected TV growth is accelerating YouTube’s share of brand advertising, a category Meta isn’t particularly into.

Amazon Ads is a silent threat most people don’t recognize. It surpassed more than $50B in annual revenue and is growing faster than either Meta or Google in advertiser wallet share, particularly in lower-funnel e-commerce, the exact segment where Meta’s Advantage+ and performance advertising is strongest. Amazon offers a unique value proposition to retail advertisers, a closed-loop where the purchase happens on the same platform as the ad. Meta can tackle this with in-app purchases, as social commerce is projected to grow exponentially in the next few years.

Even with all the risks disclosed above, and possibly mitigated, we need to take a look at the management and execution ones, such as the key-man ones, that Meta also mentions on the 10-K report. Something can happen to Zuckerberg that disables him to continue making decisions, the founder and CEO that retains 60% of voting power, and almost unilaterally decides strategic goals and capital allocation. In 2021, he decided that what we wanted was to live inside a game, a decision that lost shareholders over $80B and will be discontinued, the flagship VR metaverse platform, Horizon Worlds. This happened because no board intervention was possible.

The AI CapEx cycle at $115–135B in 2026 alone is a similar magnitude bet. If AI infrastructure doesn’t translate into measurable ad revenue uplift within 2–3 years, there is no governance mechanism to stop it.

Talent concentration in AI is a second execution risk. The Benzinga headline I showed earlier — Meta paying $250M to a 24-year-old AI researcher — illustrates the dynamic. The AI talent market is structurally inflationary, and both Google DeepMind and OpenAI/Microsoft are competing for the same people. If Meta loses ground in its AI capabilities, the Advantage+ moat erodes faster than most models assume.

And last but not the least, as of now regulatory risks aren’t a major concern but can turn into one for the reasons I’ll explain. Meta is involved in antitrust and competition cases against the FTC, for the claim of illegally maintaining a monopoly by acquiring Instagram (2012) and WhatsApp (2014). So far, courts have ruled in Meta’s favor, finding insufficient proof of monopoly power, and this will probably end like that. But it’s worth a paragraph.

On the data protection side, there are numerous ongoing investigations across Europe, GDPR enforcement led to a record €1.2B fine (2023) for unlawful EU–US data transfers. We can expect this kind of litigation to continue in the foreseeable future.

Most recently, there have been issues related to youth safety and social harm, Meta currently faces lawsuits from 33 U.S. states for the claim that platforms are intentionally addictive and harm teens. New Mexico found Meta liable to harm children and ruled a $375M penalty for the damages, due to failure in protecting minors and disclosing risks. A penalty of that amount isn’t harmful to Meta’s strong financial position, but there’s an increasing number of people suing the company for these matters, and we need to pay close attention as it can amount to something meaningful in the next few years.

Valuation

Before the DCF, let’s compare the current multiples with historical averages.

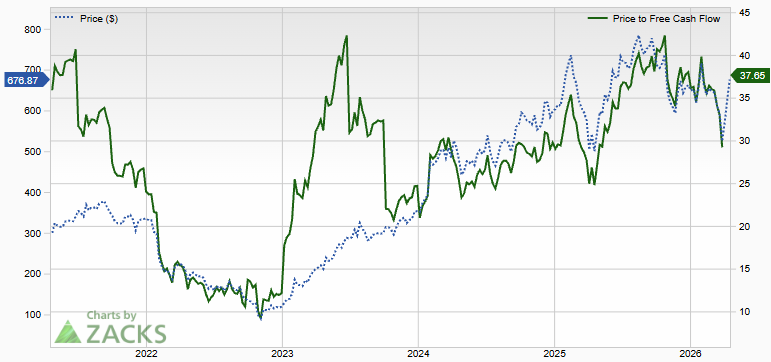

P/FCF is approaching historical highs, after briefly touching below 30 in the general market correction due to the war with Iran.

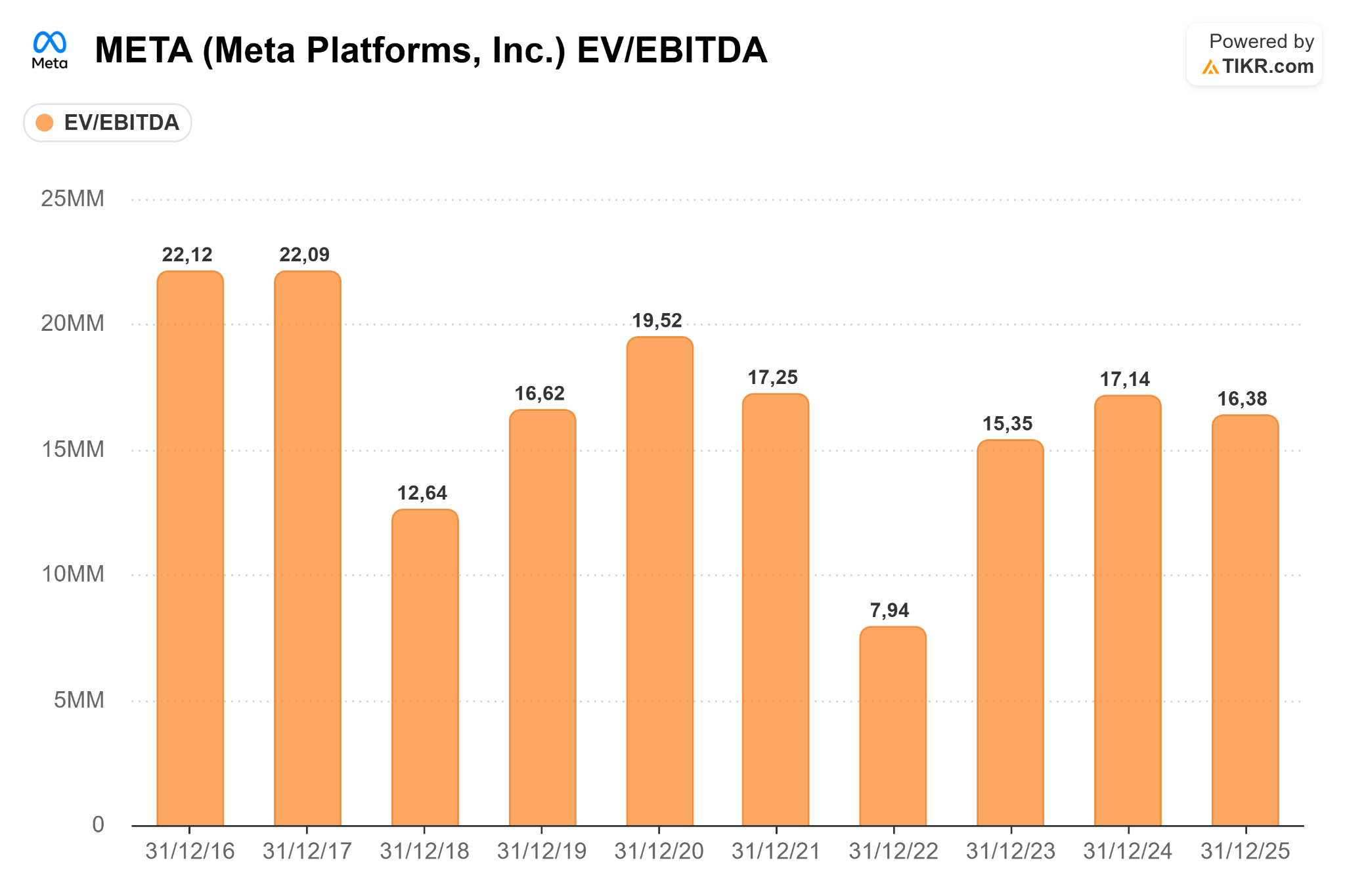

EV/EBITDA is around the historical average of 15.

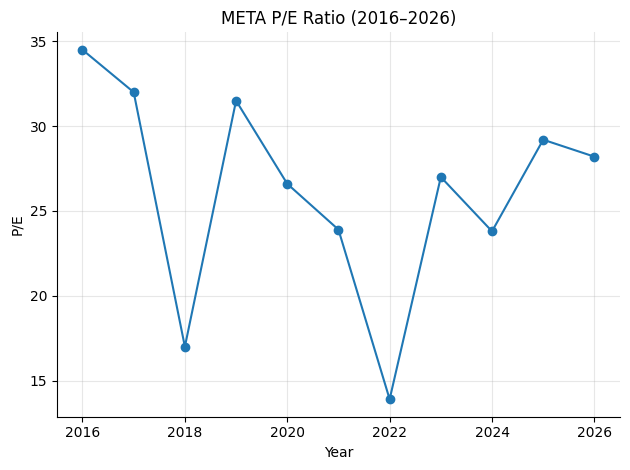

P/E ratio is also around the average, despite some dips below 20.

If we just look at multiples, Meta stock appears to be trading at roughly the fair value. Now let’s move on to a DCF with three scenarios.

Bear Scenario

Revenue growth slows to 15%, the AI infrastructure bet doesn’t pay off meaningfully, and the margins stay compressed. At that point, the stock is significantly overvalued today and the intrinsic value is in the $364-$445 range.

Base Scenario

Meta executes roughly a bit more conservatively than guidance, roughly 20% growth, and operating margins recover toward historical highs as CapEx normalizes post-2027. The stock looks roughly fairly valued, maybe slightly expensive. In this case, the fair value is in the $492-$602 range.

Bull Scenario

The AI investment cycle meaningfully accelerates monetization. WhatsApp starts contributing meaningfully, and margins push above 42%. Even then, today’s price leaves little margin of safety. The fair value is in the $573-$700 range.

Every projection assumes a WACC below 10% and a Terminal Growth Rate of 4%, which I consider reasonable due to the fact that Meta’s business model can grow non-linearly even in a mature phase, so it makes sense to put a premium on the 2-3% we usually see on most companies.

What Would Change My Mind

Despite forming a positive thesis on Meta, there are some specific points that would lead me to reconsider being a shareholder. One of them is CapEx reaching levels that would seriously scare me, not due to the volume but the way it could destabilize the solid financial condition we always knew. In FY2024, CapEx was roughly $37B, the guidance for FY2026 is $135B, a 264% increase in 2 years. In FY2025, CapEx amounted to 33% of revenue. I understand that from now on, we’ll need higher levels not only for growth but also for maintenance of the infrastructure being built. I’ll get seriously worried if it reaches a 75% ratio, spending three quarters of the year’s cash collected in infrastructure with a ROI that’s uncertain, especially if the FCF approaches negative (or near negative) territory or the debt-to-equity ratio surpasses 50%.

The last thing that I’m not too tolerant of is if the race for AI talent, mostly paid in equity, becomes a spiral that reminds us of a bubble and dilutes shareholders. Meta’s been countering this with stock buybacks, but I don’t want to see the number of shares outstanding going consistently up.

Conclusion

To conclude this deep dive, I have a positive view towards Meta’s future. I think it’s one of the companies that can benefit the most from AI initiatives, operating a business with almost zero marginal costs per new user. The market is worried about the elevated investment amount, the stock had one of its worst trading sessions when management announced this year’s guidance. I don’t share that view because Meta’s proving to be capable of supporting it without destabilizing the balance sheet and while generating positive free cash flows, even if momentarily suppressed. I consider this an opportunity to generate superior returns in the next few years, and plan to add the stock to the portfolio at the price ranges mentioned in the Valuation section.

Disclaimer: Margin Valley Research is an independent research publication focused on macro analysis and equity research. All content published on this Substack is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security or financial instrument.

The views expressed are solely those of Margin Valley Research and are based on sources believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy or completeness. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal.

Nothing published here should be construed as the provision of personalised investment advice. Readers should conduct their own due diligence and consult with a qualified financial adviser before making any investment decision.

Margin Valley Research may hold positions in securities or instruments discussed in its publications. Any such positions will not be disclosed on an individual post basis and should not be interpreted as a conflict of interest.

This publication is not regulated by any financial authority. By reading this content, you acknowledge that you do so entirely at your own risk.